Retiring Early During A Recession

A reader asks “Can you write a post on how early retirement works in a bear market (potential recession) scenario going for say 1-2 more years earning less than 10% or even say 6%. Meaning a real return of 0% as per your assumption. What kind of planning should folks who have already retired and folks who are planning can take. Keeping a good buffer is definitely one option but any other thoughts to discuss there (fixed income vs equity balance or others) will be great to see”. So lets see what it takes to be retired in this situation and if there is something we can do to reduce the impact of an unexpected long recessionary climate.

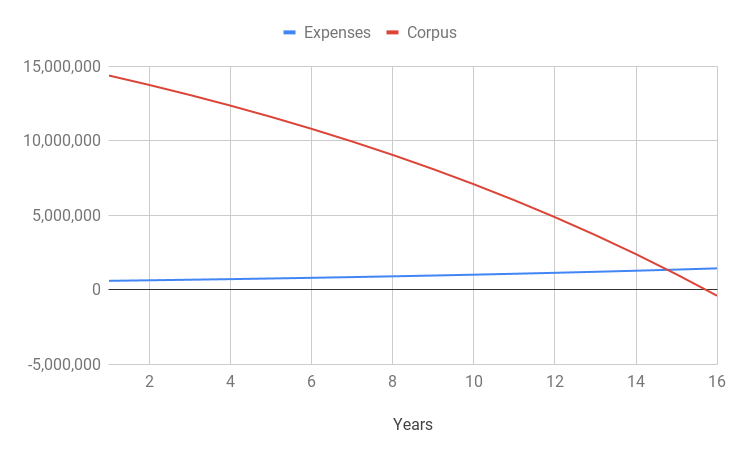

I have already done some analysis of how 4% rule works in Indian context. This is an extension of that post, so in case you haven’t read it yet, I suggest you read that first. Lets go with an assumption of 6% inflation and a 4% withdrawal rate. Assume monthly expenses of Rs. 50K, then the corpus would have to be Rs. 1.5 crore. With that kind of spending and a 0% return on investment for ever, the amount you saved up would last only 15 years. Not a good situation to be in, but at least you know that your corpus without any buffer will last you 15 years of recession.

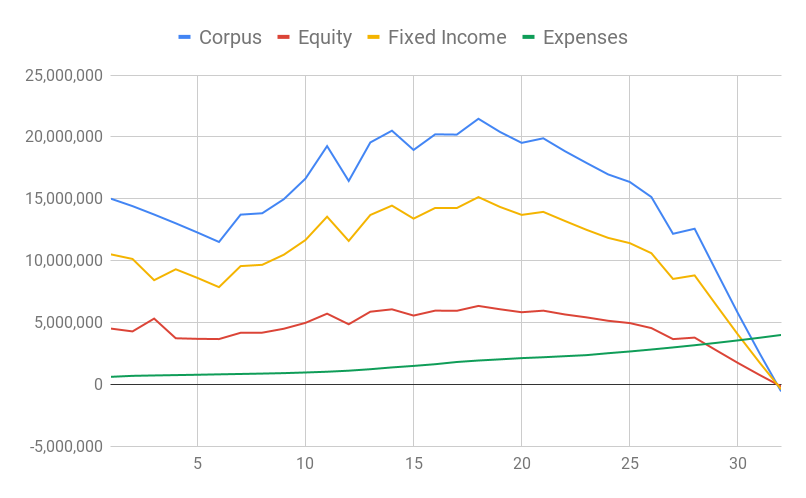

Instead, lets say, there is a 2 year recession and then the economy was back to giving you 9% return, then your investment would last 35 years. With 3 years of recession it will last 31 years and a 5 years recession will mean that the corpus will last for 25 years. The assumption here is that a recession starts right after you retire and gives 0% real return during those first 5 years.

Using real FD rates, inflation and stock market returns from 1998 onwards, except using a 0% return for the first 5 years, we arrive at the 31 years mark before which the corpus becomes zero. That is based on the assumption of 30% in equity and 70% in FDs and without any buffer and assuming history will repeat after the 5 year 0% return scenario.

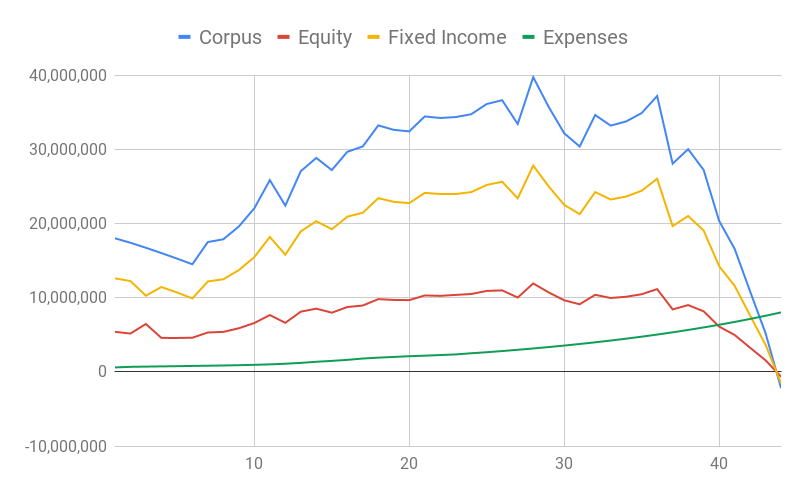

Instead, if we gave a 20% buffer, the corpus would last 43 years even if there is a 5 year recession at the start of retirement and history repeats itself in the stock market. Not too bad if you ask me. So if you retire at 37 like I did then you would be 80 before you run out of money.

But that is still excessively pessimistic. Instead, if we assume a 50% equity and FD split with a 20% buffer, the corpus would last for more than 100 years. Basically you will never run out of money even after 5 years of recession. Of course you can torture a spreadsheet to make it tell you whatever you want to see, but the reality will always be different. Don’t blindly take my word for it and do your own analysis.

Hear it from Mr. Money Mustache

Coincidentally, Mr. Money Mustache recently wrote an article on Why You’ll Probably Never Run Out Of Money which is timely. Do check it out. Many people spend too much time worrying about not having enough money and visualizing worst case scenarios instead of taking the dive. They say things like

“I think I’m close to having enough money to jump into early retirement, but not quite. So I’m just working one more year and starting one more side hustle and buckling down extra hard to be more certain.”

Here are some excerpts from his post which I found to be very true even in my case and I meet and hear from people who think in the same way.

No matter how bright their financial picture is, they always find a way to undervalue their savings and overestimate their future expenses, just in case of the unexpected.

And by tilting the balance ever further in the direction of “safety”, they forget about what should be on the other side of the scale, which is “making the most of your finite time on this lovely planet.”

This happens way more than you might think. Every week, it’s in my email inbox and my in-person conversations with people I meet.

Some suggestions

Of course not everyone can be a risk taker like me, so I would not suggest that you take the dive into early retirement if you are not very sure. The last thing you want after a retirement is regret. So here are some suggestions to help you in case you retired and are worried about an upcoming recession.

- You can always work part time after you retire. I am pretty sure you have some skill that you can leverage to earn a half decent income. It may be just 10% of your original salary, but it is still something if you are worried.

- Alternatively, if you find yourself in a recession and you think your corpus can’t sustain your lifestyle, then you can always go back to work. Just make sure you keep up to date on your skills.

- You can also try to reduce your spending. Hopefully you planned your retirement expense which includes some discretionary ones too like having a budget to buy a new laptop, car, etc every few years or so. All you have to do is extend those upgrades to much longer. Your expenses come down automatically. You can reduce going out for eating or buying new clothes etc. Every bit helps.

Remember that you can only plan so much before you have to take the risk and go for early retirement. Life is full of surprises and you cannot plan for every eventuality. Like I mentioned in my Should I Retire Early? post, not everyone needs to retire early even if you are financially independent. If you are a habitual procrastinator, you should not retire early.