Not Saving For Kid Was a Lie

I've said this several times before that I've not been saving anything for my kid. It is high time that I come out with the truth. I was lying. Well, sort of. Every year on my daughter's birthday, her grand parents from both sides gift her money. The money is not a small amount. It is large enough that they transfer the money to my account asking me to save up for her future. I guess they don't like my radical thoughts when it comes to saving for kid's future? Either way, they have been doing it since my daughter's first birthday in 2014.

The money is transferred to my account with the mandate that I should maintain separate accounting for my daughter and invest properly for her future. Fortunately, they do trust my investment skills :). During the first two years, I just invested the whole amount in a couple of debt funds under my name not knowing if this birthday gifting tradition will continue into the future or not. After the third gift, I thought I need to do proper investments under her name. Especially since it was polluting my portfolio. Moreover bookkeeping and reporting her investments to the gift givers was getting cumbersome. Thus started the process of investing under my kids name.

Creating a minor account

The first thing I needed to do was create a minor bank account. This was quite easy with ICICI's Young Stars account. I am sure other banks have similar facility. Just search for "your bank name minor account" on your favorite search engine. I submitted all the documents and a bank account on my kid's name was activated and attached to my account in a few days. The whole process was quite straightforward and quick.

Then I proceeded to create a CAN (Common Account Number) on my daughter's name using the forms available on MF Utilities. I also submitted a PayEezz mandate form so the transfer to mutual funds can happen directly from my daughter's bank. In a few weeks a CAN number was allotted to her. Now the investing can start on her name. I created an account on MF utilities online and started investing.

Investing for the kid

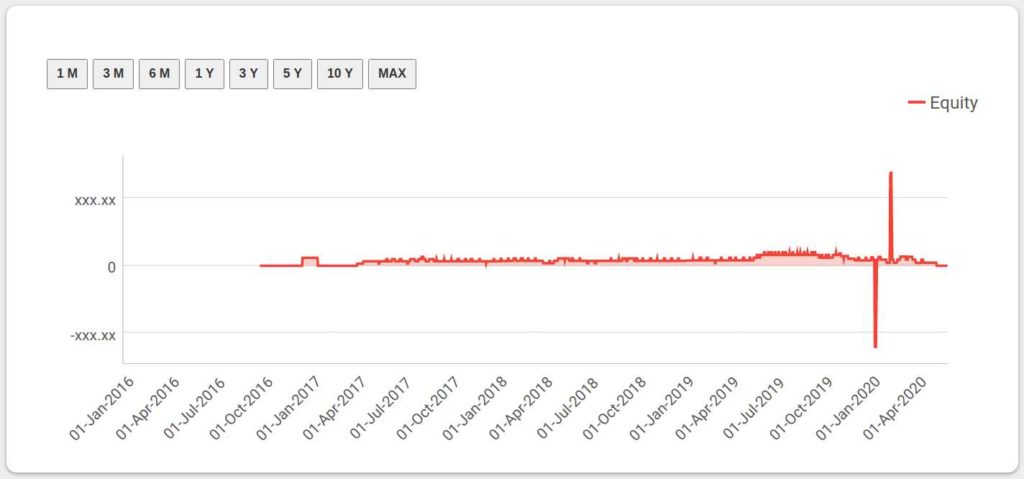

As I mentioned before, the grand parents have gifted her in 2014 and 2015 which I invested under my name. I sold that amount and invested under my kid's name into a couple of ultra short term debt funds. Initially I did not have a plan for my kid's gifts. Just wanted to move her money out of mine, so the accounting would be simpler. Hence the use of ultra short term funds. That is the initial spike you see in the chart below.

Then, much later in 2019 I finally moved all the debt investments into equity in a staggered manner. Which is what you see as the troughs in the chart above starting from April 2019. The reason I waited until April 2019 was because of taxes. You see, until financial year 2018-19, I still got salary from work, so I was in the highest tax bracket. If I sold during that time, I have to pay tax at my slab because the debt investment was short term in nature (less than 3 years since investment). So I waited until I retired and fell in the lowest tax bracket :). Anyway the equity market was not favorable.

If you notice the chart, there is a lot of empty space from 2016 to 2019 where I was not investing anything. What happened to the birthday gifts during that time? Well I was investing in equities. By the way, the charts come from the investment analysis web app that I wrote.

Equity investments experiment

I have always wondered how a portfolio would perform if you are invested 100% into equity mutual funds. I thought my daughter's portfolio could be a good playground to test out my experiment. Anyway, it is OPM (other people's money). I know, I am a little bit cynical. But the point is that I need to show the report card of my kid's investments to the grand parents. So it is not like I can gamble and not be held accountable :).

My plan was to invest completely into a couple of multi-cap equity mutual funds every time my daughter gets a gift on her birthday. Since you know I don't like lump-sum investments, I split the gifts into 12 equal parts and invest over the year. Upon receipt, the gifts first go into my wife's ultra short term funds. Then, over the year, I sell 1/12th the amount from my wife's account and invest into my kid's equity funds. I know it is a round about way of doing things, but I like to have separation of concerns. My portfolio stays clean of arbitrary transactions. And my kid's portfolio can be 100% equity all the time. You can see the equity investments in the chart below.

From 2016, I have been investing steadily every month into equities. From April 2019 to November 2019, you will see a slight bump up in the investments because I am selling the old debt funds and investing into equities. Finally you will notice a spike in January 2020. The reason was that I completely got out of a poorly performing mutual fund and invested into another one as part of my biannual portfolio check-up.

Performance

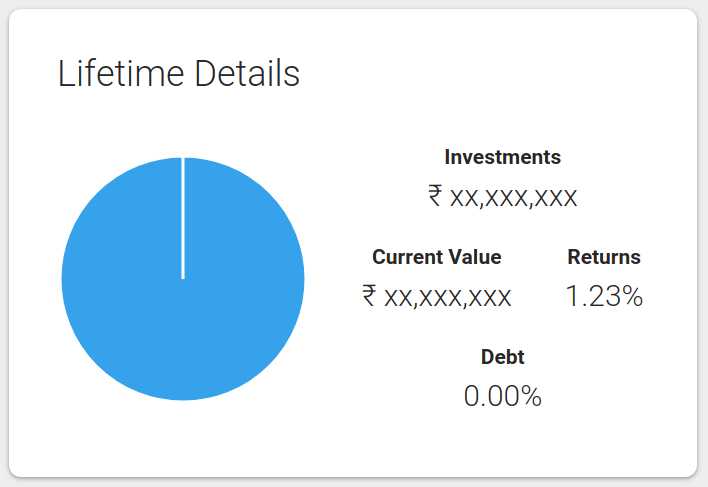

It is way too early to comment on the performance of a portfolio that is barely 4 years old. But none the less, here it is.

A 100% equity portfolio giving a return of 1.23% over a period of 4 years is quite poor really. But that is why this is an experiment and the main culprit is the recent market crash. Thankfully, the amount is sufficiently small for me to not worry about it. We will see how this experiment pans out.

Conclusion

The truth is that my kid does have a corpus. But I have always denied that didn't I? Was I lying? Well, not really :). I personally am not saving anything for her. I don't have a goal for her corpus. No higher education corpus. No marriage corpus. Nothing. I don't account her portfolio in any of my calculations. It is there because her grand parents want something on her name and I cannot take that away from them.