What Was My Savings Rate

A lot of times while talking to people about my early retirement, I get to the point of someone wanting to know what percent of my income I was saving. Unfortunately I never tracked that metric. So I wanted to find that out myself which is what this post is all about. The information may not be very accurate but it should be a ballpark figure and has sufficient details in it. The reason for inaccuracy is primarily because I don’t want to track down all my investments and income to the minutest detail. That would take too much time. In fact I don’t even remember my salary information and used my ITR (income tax returns) as a guideline. Then I had to go through my CAMS statement to figure out my investments every year. Hope this helps answer the question about my savings rate.

Savings rate

My income consists of salary, annual bonus and employee stock options. And while reading through the post remember that I have been lucky enough to have been working at a very well paying job. So my savings rate may look a bit crazy. The way I am calculating savings rate is using this simple formula

Savings rate = Investments / Post tax annual income

Post tax income is the amount after taxes have been deducted. For example let’s say my annual income including salary, annual bonus and employee stock options is Rs. 30 lakhs. If my tax is Rs. 7 lakhs, then my post tax annual income would be Rs. 23 lakhs. Now lets look at my savings rate below.

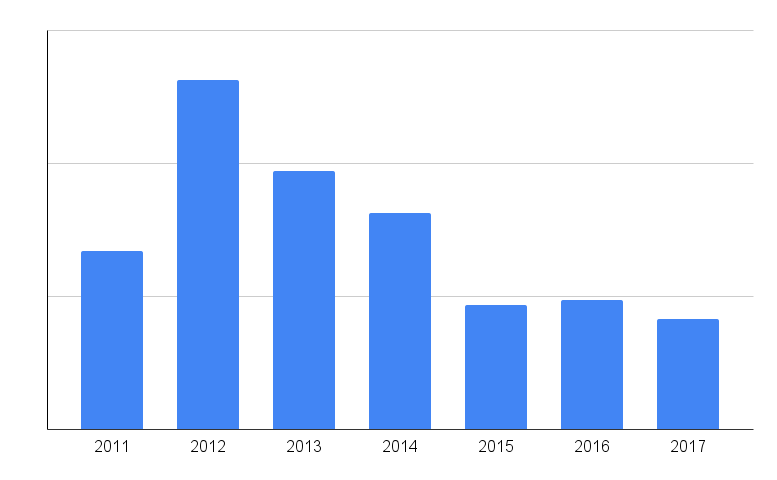

| Financial Year | Savings rate |

|---|---|

| 2011-12 | 71% |

| 2012-13 | 46% |

| 2013-14 | 75% |

| 2014-15 | 76% |

| 2015-16 | 86% |

| 2016-17 | 87% |

| 2017-18 | 88% |

So when I first started investing I was already saving considerable amount of money because I was planning to retire by 2025. There is a big dip in savings in 2012 because we moved into our newly constructed house and there were a bunch of “interior decoration” expenses. I went back to 75% savings rate in 2013 and it continued on in 2014.

Expenses

Around 2015 we were practicing minimalism and cut down the expenses even more. By 2016 I was a minimalist and a stoic. That helped us continue our crazy savings rate of 87% into 2016 and 2017. So you know how little we were spending. All our unnecessary expenses like buying electronics, clothes, eating outside etc went straight to zero. Coupled with the bull market from 2014 our corpus grew at a rapid pace. And you know the rest is history and I retired in June 2018.

In 2012, my expenses shot up as I explained before, because my house construction has completed, so had to pay all the pending bills and spent a bit on buying a bunch of furniture. Bought a second car in 2013 and we had our kid. As 2014 rolled in, our expenses normalized. From 2015 onwards, minimalism kicked in and our expenses went down further.

Things to note

You have to remember that while I was working a bunch of expenses were borne by my company including paying for my mobile device, cell phone bills, internet bills, medical expenses, gym facility, food expenses (free food), travel benefits etc. So expenses out of my pocket were not as much. As a result, don’t be alarmed to know that my savings rate is so high.

Another thing to note is that a big part of my income was automatic investment on my behalf by my employer. Let me explain. About 50% of my total income from my employer in a financial year was in the form of employee stock options and EPF. Both of which would never hit my bank account. The EPF amount goes into my PF account and the employee stock options show up as units of shares of my company in my name. So 50% of my income is automatically just saved on my behalf. If I was saving any less than 50% it means I must have used up all my salary in that year and in addition sold some stocks to pay for my expenses. Which is exactly what happened in 2012.

Real savings rate

With the above information, we could redo the numbers in a slightly different way. What would be my savings rate if I considered my income as just the money that got credited into my bank account? In that case, my savings rate will change to something that I have shown below.

| Financial Year | Savings rate |

|---|---|

| 2011-12 | 45% |

| 2012-13 | 18% |

| 2013-14 | - |

| 2014-15 | 63% |

| 2015-16 | 75% |

| 2016-17 | 75% |

| 2017-18 | 55% |

I did not calculate my savings rate for 2013 because I made a lot of transactions like selling my US employee stock options and buying mutual funds in India. I did not want to make all the complex calculations, but you can imagine it to be around 50%. Finally, in 2017, the savings rate seems a little bit lower although my expenses were lower than 2016 is because I was on sabbatical during that period and hence I was not paid any salary for some part of the year.

Conclusion

No matter how you slice and dice, my savings rate has been at least 50% for the most part of my pre-minimalist life. Once I became a minimalist, the savings rate has been around 80%. The only reason it was possible is because I was earning a good salary and minimalism helped my case too. So now you know why I was able to retire so early. Remember also that my company provides employees with a lot of benefits, so my minimalist expenses while I was working were lower than my current expenses!

For your case I’d suggest that you try and maximize your savings and minimize your expenses. Don’t bother too much about the savings rate. If you are doing your best, then that is good enough. Since an early retirement goal does not have a deadline, you just have to continue saving until you reach your goal.