Asset Allocation Explained

In my earlier post on How to Retire Early in Five Steps, I briefly touched upon asset allocation in step #3. In this post, I go into a bit more detail into how one should go about asset allocation for early retirement. Before understanding asset allocation, you need to understand asset classes. If you have not read my post on asset classes, head on over to that post.

Disclaimer: The asset allocations discussed here are only a suggestion, it may or may not work for you because your needs and requirements may be different from mine. Please work with your financial planner if you are not sure.

What is Asset Allocation

Wikipedia defines asset allocation as

Asset allocation is the rigorous implementation of an investment strategy that attempts to balance risk versus reward by adjusting the percentage of each asset in an investment portfolio according to the investor's risk tolerance, goals and investment time frame.

-- Wikipedia

In simple terms, it is a way you allocate your investments to various asset classes such that the investment's risk matches with your risk appetite. For example, investing all your money in stocks is a high risk endeavor, but you stand to gain a lot too because the returns on equity is huge (about 20%). But what if you are risk averse and may not be able to sleep if your investment drops by 75% in a matter of months? May be you choose to invest everything in fixed deposits to reduce risk, but then you will also have poor returns (around 8% if you are lucky). What are you to do?

Depending on your risk appetite, you may want to invest different percentages of your investment into different asset classes. And that is asset allocation. When you search online for asset allocation, particularly between debt and equity, you see a lot of people suggest investing 100 - your age percent in equity and the rest in debt. So if you are 25 year old, you should invest 75% in equities and 25% in debt funds. And later in your life, you will keep moving the ratio in favor of debt funds. For example when you are 60, you would have 40% invested in equities and 60% in debt funds. The reason is because you should be reducing risk as you near your retirement and beyond, and equities are associated with risk (and rightly so). But this does not work for early retirement.

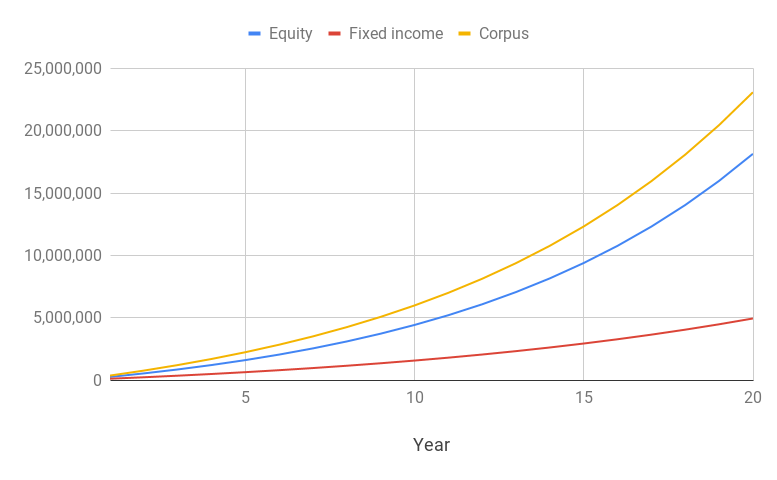

Instead, this is my suggested asset allocation (if you have read my previous post, you know that I only consider cash, fixed income and equity mutual funds to be the only useful asset classes).

- Cash: Keep 3 months worth of expenses in your bank. Expenses should include household expenses, rent, EMIs, monthly bills, school fees etc. If you want to be more cautious, save up to 6 months worth of expenses. You will use this money in case of any emergencies like losing a job or medical emergency etc.

- Fixed Income: Allocate 30% of your investments into this asset class. That 30% should include all fixed incomes including any FDs, PFs, PPFs, NPS, Debt Mutual funds etc. When investing in debt mutual funds, consider investing only in ultra short term or short term debt mutual funds. If you know what you are doing, and can take interest rate risk, then invest in Gilt funds.

- Equity: Allocate 70% of your investments into this asset class. I don't have any specific recommendations here, but don't invest in stocks directly unless you know what you are doing (most people don't). Based on your risk appetite, you can go for a mix of multicap, smallcap, midcap and largecap funds (another post on this). If you want to keep things simple, just invest in 2 to 3 multicap funds and 1 or 2 ELSS funds (if you have not already maxed out your section 80C deductions).

So, every time you want to invest, you can simply invest 70% of it in equity and 30% in fixed income. But what if the stock market was very favorable and the equity ratio of your corpus now becomes 80%? Well in that case you have 2 options

- Start investing more into fixed income, and less into equity next month on wards so as to bring the ratio back to the way it is supposed to be. For example, invest 30% in equity and 70% in fixed income every month until the ratio of your corpus comes back to 70:30.

- Sell from the asset class that has gone up and move it into the other asset class. Going with the current example, you would sell 10% of equity and invest in fixed income to bring the ratio back to 70:30. I would not suggest this option because the re-balancing can cause taxable capital gains. Moreover, tax filing becomes a headache because you will need to find all the taxable events and report it.

The whole point of investing in this style is to buy assets when they are cheap, depending on cycle for the asset. For example when markets are high, the risk of a market fall increases, but that also means that you corpus would have skewed towards equity and you will start investing more in fixed income and less in equity, which means you are buying the cheaper asset and ignoring the expensive one. Likewise, when interest rate increases, fixed income will look expensive and also have a bigger ratio in your corpus, as a result you will be buying more equity which would have been beaten down due to high interest rates. Again you are buying the cheaper asset (equity).

This idea of asset allocation works when asset classes are negatively correlated. Equity and debt have a slight negative correlation in the long term, just like inflation and gold have a negative correlation. So when one asset class goes up the other comes down (becomes cheaper) and that is when you should be buying more of the cheaper asset. The 70:30 allocation will keep you on track.

The only requirement for this to work is that you should keep investing every month irrespective of market conditions or how your portfolio is doing. Just keep investing until your corpus becomes big enough for you to retire. Use the How Much Do You Need To Retire Calculator to determine how big your corpus should be.