Reducing My Asset Allocation Swings

Ever since I started investing back in 2011, I have always wanted to do tactical asset allocation. The idea was not to maximize returns, but to minimize volatility. Tactical asset allocation is different from the general advice which you receive from many people including me which is to keep a fixed asset allocation and rebalance once in a while to make sure that the asset allocation difference remains within a small range. That advice applies for any long term goal like retirement. For shorter goals you may receive advice to reduce equity allocation as you near the goal. If I did not make any sense there, then let me explain with an example.

Let’s say, you or your financial planner decided that you should go with a 60%, 30% and 10% asset allocation to equity, fixed income and gold respectively. It is just an example and varies from individual to individual depending on their goals and risk profiles. Initially when they first start investing, they could be dividing their savings into these three buckets in their respective ratios. So if your salary is Rs. 1L and you intend to save Rs. 50K, then Rs. 30K goes into equity investments, Rs. 15K goes into fixed income and Rs. 5K goes into gold. That brings your asset allocation to the 60:30:10 split that you wanted.

Now, as time goes by, some assets move faster than others and some can go negative as well. So you keep monitoring the ratio as you continue investing every month. Eventually the ratio would have changed sufficiently that you will need to bring them into balance. Continuing on with the example above, lets say the ratio changed to 65% equity, 27% fixed income and 8% gold then you will need to sell 5% investments in equity and distribute that to fixed income and gold to maintain the original 60:30:10 ratio. That is called rebalancing.

That example was for a fixed asset allocation. What I do is tactical asset allocation. Before I explain it, you should know that I have only two asset classes, equity and fixed income. I did not go with a fixed asset allocation like 70% in equity and 30% in fixed income because I wanted to play the market a bit. My plan was to change the asset allocation anywhere from 30% all the way to 70% allocation to equity and the rest to fixed income depending on my reading of market conditions. So if I felt that the stock market is too high, I would go with 30% allocation to equity and vice versa. However there is a problem with this approach.

The problem is that every time I have to change the asset allocation by such wild swings, I would have to buy and sell a lot. Take for instance, say right now I am at 75% equity allocation. If I was going with a fixed allocation, I could sell 5% of equity and buy 5% of fixed income to keep 70% equity and 30% fixed income ratio. But lets say I feel the market is too high and I should really be at only 50% in equity. With this strategy, I will have to sell 25% of equity and buy 25% of fixed income. When I had a small investment, this was not a problem. To make it more concrete, lets say I have Rs. 10L invested with an allocation of Rs. 7.5L in equity and Rs. 2.5L in fixed income. To change the asset allocation to 50:50, I need to sell Rs. 2.5L of equity, pay tax on it and invest the rest (post tax) into fixed income.

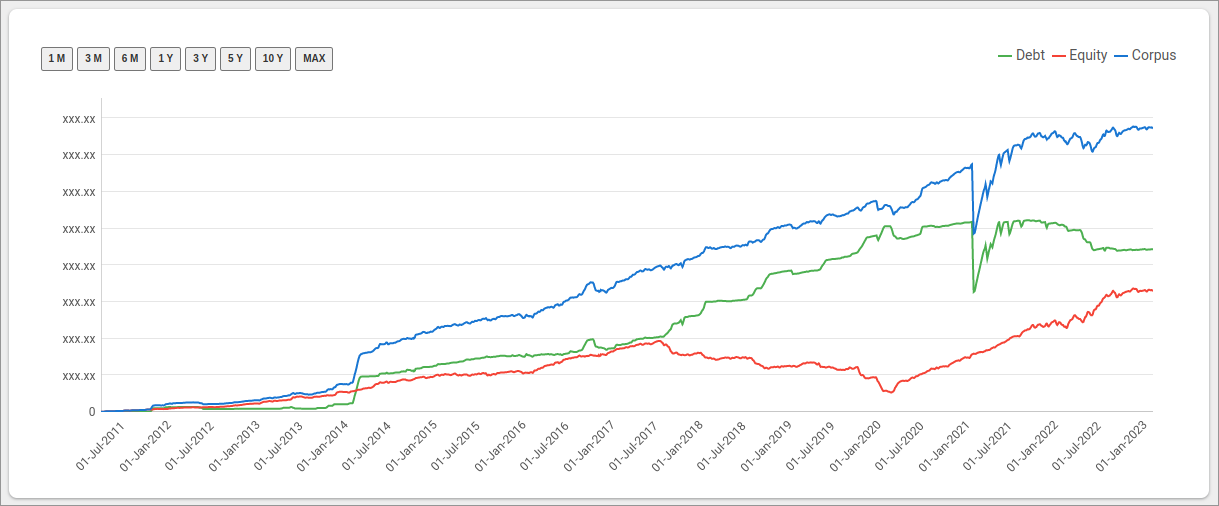

But with large amounts, the tax could be huge. Let’s take another concrete example. Say I have Rs. 100L investments of which Rs. 75L is in equity and Rs. 25L in fixed income. Now to balance to 50:50, I will need to sell Rs. 25L from equity and pay tax on it and invest the rest in fixed income. I happily sold and bought such huge amounts up until 2018 when there was no tax on capital gains on equity. Which means, even if I sold Rs. 25L, I needed to pay Rs. 0 in taxes until 2018. But the budget changed things and made equity also taxable. So now I am wondering if this tactical asset allocation is a useful strategy or not given the taxes. You can checkout my asset allocation in the past in the chart below.

I haven’t yet decided what I will do yet, but most likely I will settle with a fixed 70:30 equity to fixed income asset allocation whenever I reach that allocation. I will most likely not apply any tactical allocation going forward. That is my thought process as of today, but it may change again in future :). The only constant is change as we all know. One of the downside of a fixed asset allocation is a bit more volatility, but I guess that is easier than figuring out taxes and shuffling a lot of money around. If my strategy were to change again, I will certainly let you know.