Capital Gains Harvesting

A couple of weeks ago, I mentioned about tax loss harvesting being a legitimate way to reduce your taxes. In this post, I will explain another way to reduce taxes while taking capital gains using capital gains harvesting. A capital gain harvesting is basically a method of tactically selling some of your investments for capital gains without actually paying any taxes on them. How does that work? Let’s find more about it in this post.

One simple capital gains harvesting technique which pretty much everyone should use to their advantage is in equity investments. Basically, you don’t have to pay any taxes on long term equity capital gains up to the limit of Rs. 1 lakh in a financial year. So you stand to benefit by selling your equity investments until you realize Rs. 1 lakh worth of long term capital gains. Then you invest the amount you sold back into the same investment vehicle.

Let’s take an example. Say, you invested some Rs. 10 lakhs into an equity mutual fund. It has been more than a year ago since you invested in the fund. Now the value of your investment is Rs. 11 lakhs. Then you sell all of it. Which means you will be sitting on a capital gain of Rs. 1 lakh. Then, you invest back the full Rs. 11 lakhs that you sold back into the same mutual fund. When you are filing taxes, you will report the Rs. 1 lakh long term equity capital gain, but you will not be charged any tax on that because of the tax break.

So in the end, your investments haven’t changed. You still have Rs. 11 lakh investment like you had earlier, yet the cost of acquisition is now Rs. 11 lakhs instead of Rs. 10 lakhs. That means any future capital gains will be lower by Rs. 1 lakh. To help understand, lets continue with the example. Let’s say, next year, the value of the investment grew to Rs. 15 lakhs and you wanted all that money for some purpose. Assuming you did not make use of the capital gains harvesting, you will have a capital gain of Rs. 15 lakhs - Rs. 10 lakhs (your original investment) = Rs. 5 lakhs. Out of that, Rs. 1 lakh is tax exempt and you pay tax on the rest of Rs. 4 lakhs at 10% tax (the prevailing rate for long term equity capital gains at the time of writing this post). You pay Rs. 40,000 tax and you are done.

Now lets take the other scenario where you have done capital gains harvesting. Then your capital gain is Rs. 15 lakhs - Rs. 11 lakhs (the new cost of acquisition because you sold and bought at the new price) = Rs. 4 lakhs. Out of that, Rs. 1 lakhs is tax exempt and you pay tax on the rest of Rs. 3 lakhs at 10% tax. So you have to pay Rs. 30,000 tax instead of Rs. 40,000. Imagine if you took advantage of capital gains harvesting every year, then your tax could be even lower.

This is something I do pretty much every year to reduce future taxes. But this is not all there is to capital gains harvesting. In fact you can do the capital gains harvesting with short or long term gains, with both equity and fixed income investments. The only requirement is that your income should be less than Rs. 5 lakhs where no tax is applicable. It can be higher if you take sec 80(c) benefit. It is actually Rs. 7 lakhs if you use the new tax regime from next financial year and play the numbers carefully. How will that work?

Again lets take a simple example. Say you have no income, like me since I am retired and I don’t have any income at all. No salary, no FD interest, no rental income, nothing. Suppose you invested Rs. 50 lakhs in a debt mutual fund 2 years ago. Now it is worth Rs. 55 lakhs. You sell all your investments and buy it back again. Then you realized a short term capital gain of Rs. 5 lakhs which is added to your income and taxed at the applicable rate. Since you have no other income, all of that is tax free and your investments are starting with a new higher cost of acquisition. That means your future taxes will be lower like I showed in the example earlier.

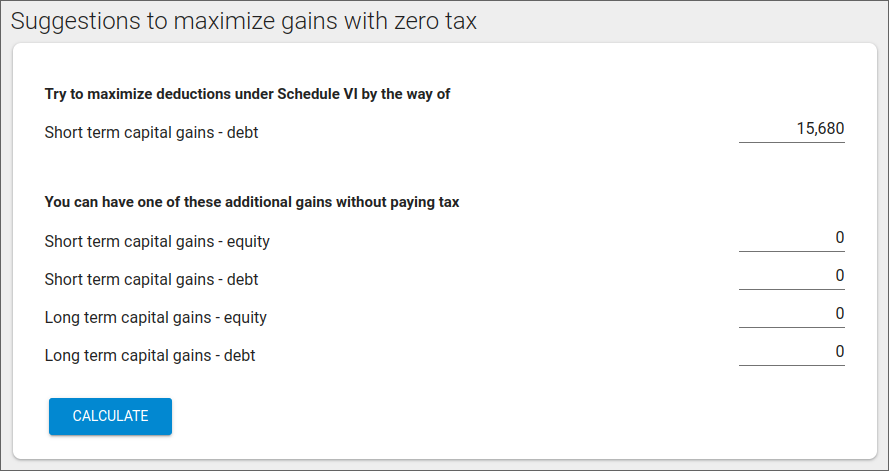

You can do the same for other capital gain combinations (short and long capital gains of both equity and fixed income). I take advantage of this kind of harvesting since I have no income now that I have retired. But it may not work for everyone. In fact I wrote a small web app that tells me in realtime exactly how much I should be selling in a financial year to maximize my capital gains harvesting based on what I have already sold (see screenshot below). Yes this is one more of those hobby projects that I keep talking about and love to work on after having retired :).

Thanks to the app, I don’t have to keep calculating how much to sell. As of now the screenshot is showing most of the numbers as zero because I already harvested most of the capital gains. We are is March. You know that we are already at the end of the financial year don’t you? So I already harvested most of my gains. Just another few thousands to sell in short term debt mutual funds before the end of this financial year.

One other note is that I don’t sell and buy in one bulk transaction. I sell a bit say Rs. 1 lakh in a day and buy the same investment (mutual fund) the same day. And I repeat that every few days. The way I execute it is by using the money from my emergency fund which is basically in my savings account, so I always have some money ready. Some sell transactions like equity mutual fund redemptions can take more than a couple of days especially if there are holidays or weekends. So make sure you can survive the dip in emergency fund for those few days.

Just remember that all the buy and sell transactions attract a stamp duty of 0.005%. So if you sell Rs. 11 lakh and invest the same again, then you will be losing Rs. 55 (for sell transaction) + Rs. 55 (for buy transaction) = Rs. 110. But that is a small expense compared to how much you can save in taxes, which is Rs. 10,000 per year if you just consider long term capital gains from equity.