How Is 4% Rule Working Out For Me?

I ended the previous post with a resounding “yes” for the question on whether 4% rule works in India or not. I also mentioned that given what we know about current inflation and return expectations in India, we can assume that the investment will last about 50 years assuming a conservative 30% asset allocation. In this article I want to show you how my portfolio was performing because I retired based on 4% rule with a bit of a buffer. So how is that working out for me? Given the market correction in the past few months and the increasing inflation, am I draining more money than I expected and am I at risk of out living my corpus? Lets find out.

Before we get into the meat of the analysis, I want to preface by saying that I became financially independent around end of 2017 and officially retired around mid 2018. So we are really looking at just 4 years worth of data which is a very short duration to make any conclusions about whether 4% rule works in real life in Indian context. Take all my conclusions with a pinch of salt. Moreover, depending on your lifestyle and risk tolerance, you might need to make some adjustments and not read too much into anything I say here. Do your own personal planning properly before jumping ship.

Inflation

Everybody’s inflation will be different and no matter what the government published numbers may suggest, it will definitely be not what you will be experiencing. In my case, as on date, my inflation is about 7.6% as compared to my expenses in 2018. It is a bit higher than what I was anticipating in retirement, but I am not particularly worried about it. I still believe it will converge to my planned 6% in the long run.

Expenses

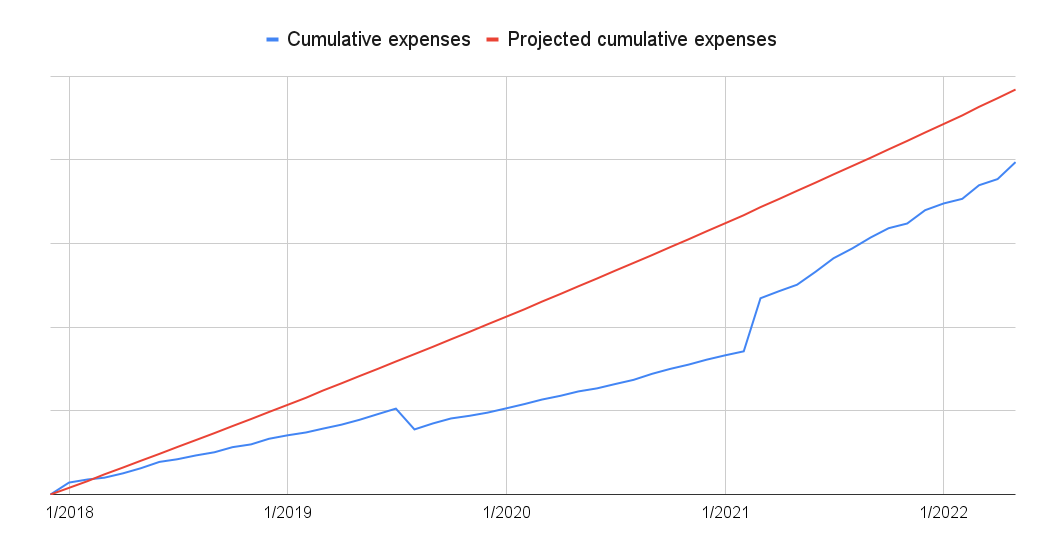

My planned expenses per year after retirement was Rs. 9.6 lakhs increasing by 6% every year. However, I have consistently been spending less than that every year as you can see in the chart below. I plotted my cumulative expenses compared with projected expenses with 6% inflation. Of course in the future when I upgrade something like buying a new car and sell my old car then the expenses will shoot through the roof. As I mentioned before, 4 years in retirement is a very short duration to capture all the major events in life.

Corpus

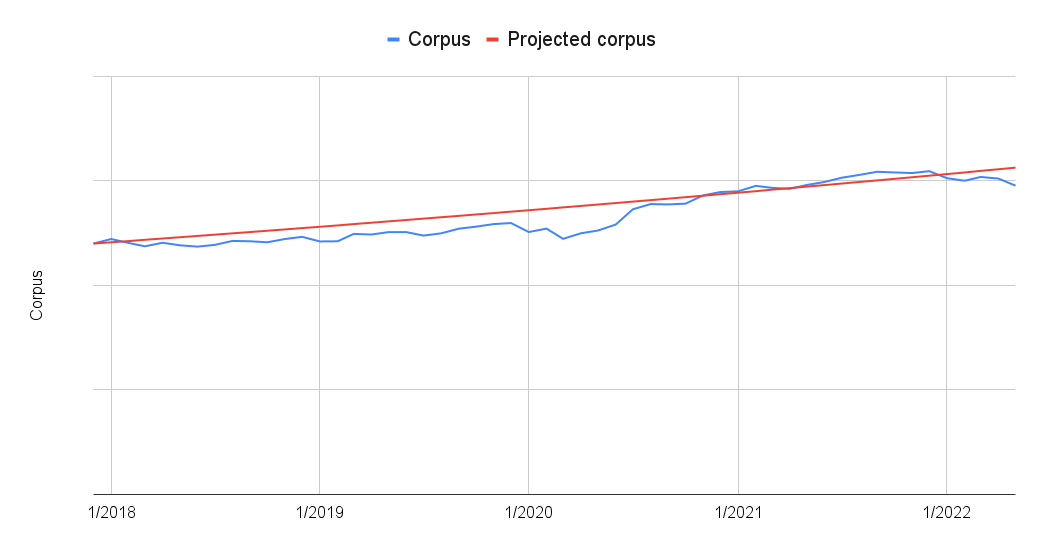

Here is where things get interesting. Now we all know that going by the 4% rule, I should have accumulated 25 times my annual expenses as my retirement corpus. In reality I have a bit more than that. But just for the sake of analysis, lets assume I saved up exactly 25 times my planned annual expenses. Then if I make a projection and compare with my real corpus (scaled to the 25x number), then it would look like the following –

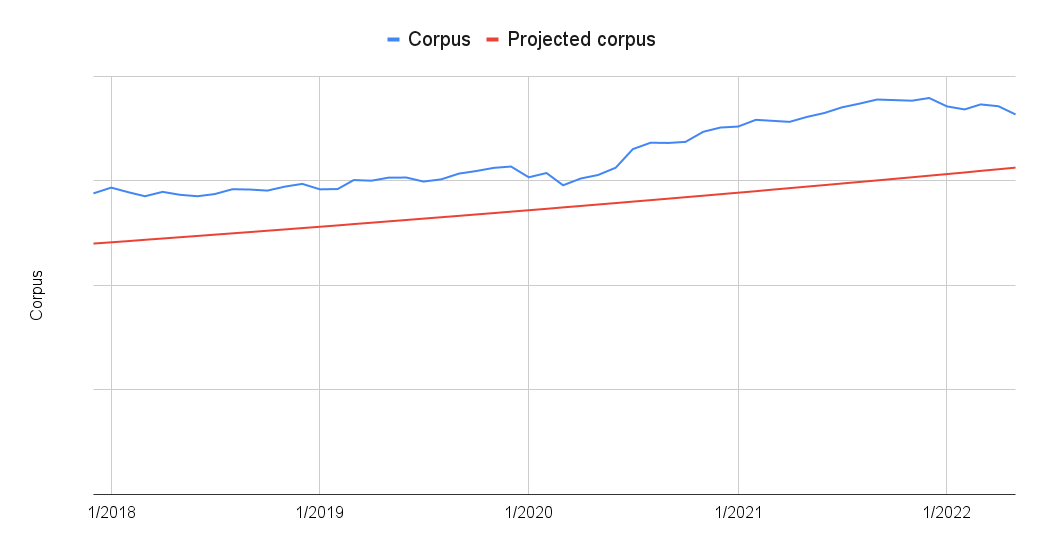

The projection is based on a 10% growth of corpus after a 6% inflated expenses deducted from it. As you will note, the real corpus line is more or less inline with the projection for the most part except for that bad period in 2020. Thanks to the latest drop in equity as well as debt mutual funds, the corpus is a bit lower than the projection, but I would not be worried. However, remember that these are based exactly on 4% rule. What would it look like if there was a 20% buffer? You will find the answers below.

So even with the down market of the recent past, I am sitting comfortably above the projected line. At least as of now 4% rule is working fine with or without a buffer. We will just have to wait another 30 years to really be sure of it though :). I was never worried about my corpus or my projections and that still continues even in the face of recent turbulence in stock markets. Although I don’t think the markets are that turbulent really. There is still more pain to come. One thing to note is that I follow a dynamic asset allocation strategy which reduces the volatility in my corpus.