Is It The End Of 4% Rule Then?

I have written so many articles on 4% rule, that it feels like I can make a living by just writing about it. Yet we keep coming back to it because times have changed, or may be the 4% rule does not work in Indian context or because it may not work during recession and what not. The latest in this saga is this article I read a few days ago. Without going into too many details, the article suggests that a new research found that the 4% spending rule may be too high and we should probably go for a 1.9% rule instead. That sucks. I made my whole early retirement planning based on the 4% rule and it seems like I may be doomed.

What is this study that puts a damper on our dreams of early retirement? It seems a new research was conducted with a more realistic assumptions about our life expectations and a more comprehensive historical data set to arrive at the 1.9% rule. So in an Indian context where a corpus of Rs. 150 lakhs would have sufficed to live a reasonably long life with Rs. 6 lakhs of annual expenses under the 4% rule, will now have to be revised to Rs. 315 lakhs under the 1.9% rule. That is a significant jump in the amount of corpus you need to build for retirement. It is more than twice the amount!

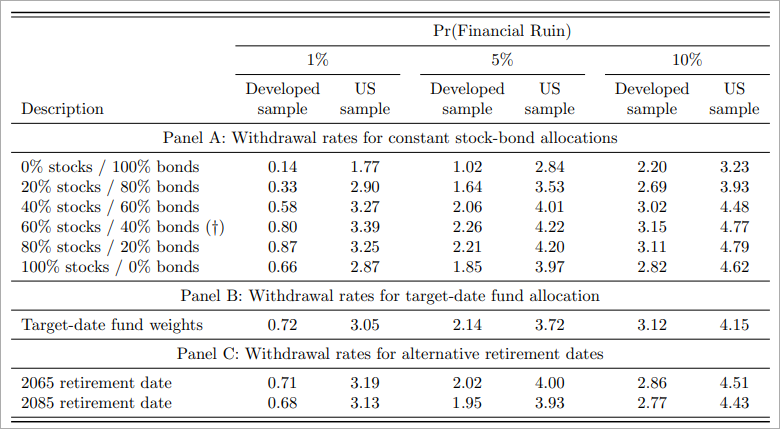

By the way, this study was conducted by professors and PhD students from the University of Arizona where I completed my Masters :). Go wildcats! The original 4% rule comes from a study done in 1994 which suggested that a 50:50 investment in equity and bonds would last for 30 years in the US based on the data available from 1926 and 1991. The new study used a longer life expectation number given the current advancements in medical field. On top of that, they also used a more comprehensive historical data of stocks, bonds and inflation numbers. They used data from 38 developed countries between 1890 and 2019. Unfortunately we still don’t have any study done on the emerging markets such as India.

Anyway, if you are worried about the 4% rule, now you can go for a more conservative 2% rule. I still trust that 4% rule will work fine and am not even slightly deterred by the study. Don’t take the numbers at face value by just reading the article. Read the actual paper in full and then come to your own conclusions. If you read closely (see table below), the 4% rule would still work in the US with a 60/40 equity/bond asset allocation. It is only when you mix in all the other countries, the results are not as good. I guess the assumption of the paper is that the US may not continue to enjoy the same fabulous returns of the past and there is a possibility in the future that it might behave like the average of all the 38 developed nations.

In fact if you just look at US returns and apply the 60/40 asset allocation, for a person retiring in 2022, it would seem that a 4.22% rule will work with a 5% chance of financial ruin. Which means you will need even less of a corpus. As I always say, you can torture any data enough to make it look the way you want :). Take everything with a pinch of salt.