Tax Audit

I was recently audited by the Income Tax Department and thought that the whole faceless scrutiny process was interesting. So here is something about it. It seems like I was one of those people who got randomly selected for Limited Scrutiny (Computer Aided Scrutiny Selection). It was the government's way of testing out the e-Proceedings facility.

Here is the email I received from the Income Tax Department.

Dear Taxpayer,

Thank you for filing your return of income for Assessment Year 2018-19 vide Ack. no. XXX on XXX.

While acknowledging the care and diligence you may have taken in preparing the return, there are certain issues which need further clarification, for which your return of Income has been selected for limited scrutiny and such issues are as under:

i. Foreign Financial Interest

In view of the above, you may submit or cause to be submitted any evidence on which you may rely in support of your return of income on the above mentioned issues to the NeAC electronically in 'e-Proceedings' facility through your account in e-Filing website (www.incometaxindiaefiling.gov.in) at your convenience on or before 15 (fifteen) days from the date of receipt of notice.

In course of assessment proceedings, if required, specific questionnaire(s) or requisition(s) for information/ document may be issued subsequently.

A brief note on 'e-Assessment Scheme, 2019' is enclosed for your kind reference. In case you require any assistance in filing your response, you may contact toll free Call Centre number 1800 103 4215.

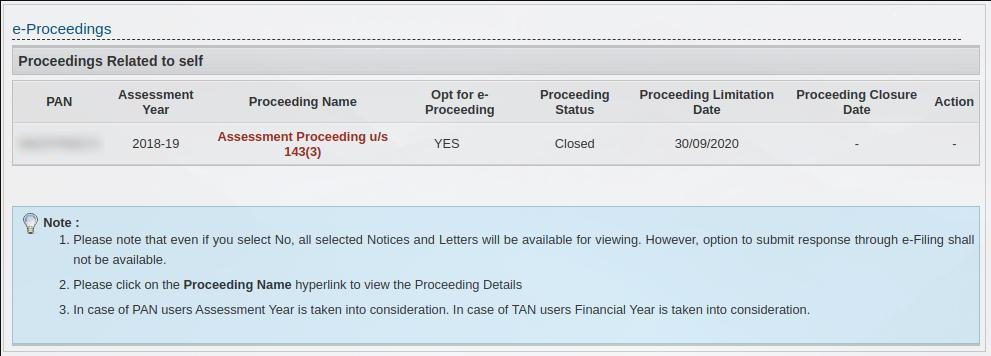

I received this email on September 29, 2019 for Assessment Year of 2018-19. Which means the scrutiny is for the previous year's filing. Strange that they are reviewing a tax filing done more than 1 year ago. Moreover the audit is about my foreign investments. Well as you probably already know, I have US stocks because I worked for a US company and I did not invest anything. Those were just stock options from my company. Anyway, I proceeded to the e-Filing website and uploaded the details of my foreign investments. It was quite a simple process really. Once you open the e-proceedings section you will see your case.

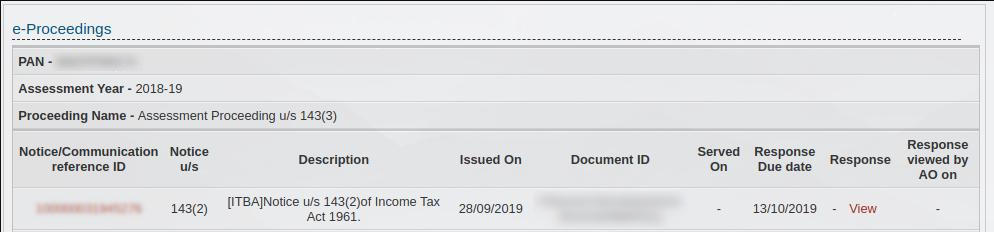

Upon clicking on the link you will reach the next page where you can submit your response in a free form text. You can also upload any supporting documents at the same time. Since I did not know what they wanted I just replied back saying that I did not invest in the stock, but received them as compensation at work. While the email said I need to respond with in 15 days, there is no date specified for how long the taxman can take to respond. So I waited and waited.

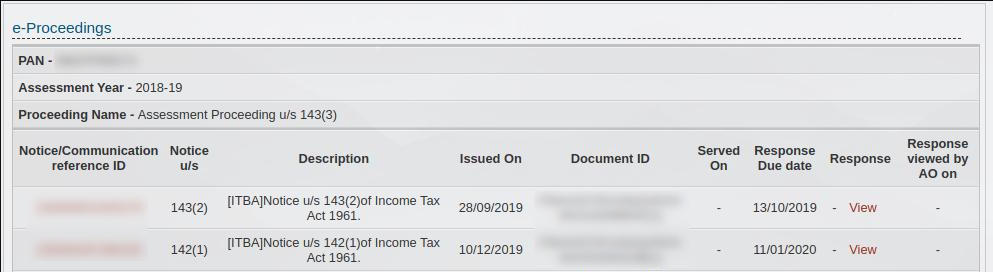

Eventually after two and half months they responded with another email requesting for more information.

Dear Taxpayer,

Kindly refer to notice u/s 143(2) of the Income-tax Act, dated 28/09/2019 for A.Y 2018-19 for conducting assessment proceedings under E-assessment Scheme, 2019.

You are requested and required to kindly furnish or cause to be furnished on or before 25/12/2019 by 11:00 AM, the accounts and documents specified in the Annexure to this notice.

The accounts or documents, as mentioned above, are required to be submitted online electronically in 'E- proceedings' facility through your account in e-Filing website (www.incometaxindiaefiling.gov.in)

Your case has been selected for scrutiny for the following reasons:

“Foreign financial interest “

With respect to the foreign financial asset in nature of investment during the year under consideration, kindly submit the below specified details:

1. Furnish details of new foreign asset in the nature of

any other asset as per schedule FA along with acquisition documents.

2. Furnish the source of investment in new foreign asset along with documentary evidence in support.

3. Please provide the cash flow from 1st April to the date of investment in respect of new foreign asset.

4. If the source of investment is not self financed, please provide the details of bank/company/individual who has financed the investment along with supporting documents.

Please note that non-compliance to this notice will lead to initiation of penalty u/s272A(1)(d) for failure to comply with the notice u/s 142(1), (Rs. 10,000/- for each default)

As usual, I responded and this time since they had specific requests about source of income, I also had to upload supporting documents. Fortunately, I kept all the documents from my past work, so it was easy. Every year during appraisals we would be handed a printout and a soft copy of the revised salary and stock options. So I uploaded those letters to indicate that I did not purchase any stocks in the US, it was just stock options from my employer. So readers, be forewarned, and keep all your documents. You never know when the taxman will ask for proofs.

After uploading my documents, I played the waiting game again. Perhaps it will take another 2 months? Well almost. After about one and half months I finally got another email on Jan 28, 2020. Seems like they were satisfied with my proofs and the scrutiny ended there. This was the email I received.

The case was selected for Limited Scrutiny assessment under the E-assessment Scheme, 2019 on the following issues:-

i. Foreign Financial Interest

After taking into account all relevant material available on record an Assessment is hereby made without making any modification to the returned income and the sum payable or refund of any amount due on the basis of the assessment is determined as per the notice of demand.

Appreciate your cooperation in the faceless e-assessment proceedings under E-Assessment Scheme, 2019.

Phew! That was the end of the scrutiny after exactly 4 months! But that was not the end of it. In the same email I also received a tax demand notice for Rs. 105.

Subject: Notice of demand under section 156 of the Income-Tax Act, 1961

1. This is to give you notice that for the assessment year 2018-19 a sum of Rs. 105, details of which are given on the reverse, has been determined to be payable by you.

2. The amount should be paid to the Manager, authorised bank/State Bank of India within 30 days of the service of this notice. A challan is enclosed for the purpose of Payment.

3. If you do not pay the amount within the period specified above, you shall be liable to pay simple interest at one per cent for every month or part of a month from the date commencing after the end of the period aforesaid in accordance with section 220(2).

4. If you do not pay the amount of the tax within the period specified above, penalty (which may be as much as the amount of tax in arrear) may be imposed upon you after giving you a reasonable opportunity of being heard in accordance with section 221.

5. If you do not pay the amount within the period specified above, proceedings for the recovery thereof will be taken in accordance with sections 222 to 227, 229 and 232 of the Income-tax Act, 1961.

6. If you intend to appeal against the assessment, you may present an appeal under Part A of Chapter XX of the Income-tax Act, 1961, to the CIT (A),Bengaluru- 12 within thirty days of the receipt of this notice, in Form No. 35, duly stamped and verified as laid down in that form.

I did not want to appeal. In fact I did not even bother to check if the assessment was correct or not. Why bother? Just pay the paltry sum :). So I logged in online and there I went into e-File >Response to Outstanding Demand to check for the tax demand. Did not find any. Waited a couple of days and checked again. There it was. One outstanding demand for Rs. 105 with challan. I just clicked it, filled in the details and paid through net-banking. I received an acknowledgement page, but no other email correspondence. Anyway, I kept checking e-File >Response to Outstanding Demand for a few days and eventually the demand disappeared confirming that the government received it's dues :)

Overall it was a pleasant experience and kudos to the government for bringing such a simplified faceless scrutiny process. It is inconvenient to meet the assessing officer directly and furnish all the details each time. The faceless process does away with it. Well in some cases you will have to visit the AO, but most can be resolved online I hope. One thing I did not like about the process is that there is no feedback from the department. No email confirmation about anything. It does not even show if and when the AO opened and checked my response although there was a column designated for it. Anyway did any of you get selected for the random scrutiny? Do let me know in the comments section below.