Risks Of Wrong Financial Planning

It is now more than 2 years since I officially retired. But unofficially I have retired in Jan 2018. I had accumulated the required retirement corpus by Dec 2017 and I could retire at the beginning of 2018. But for reasons best described in one of my earliest posts, I decided to delay my retirement date by 6 months. The way I decided when I was ready to quit was based on the 4% rule. Since it's been only 2.5 years, I can't say for sure if the 4% rule is working or not. We will have to wait and see at least 10 years really. But ideally you will have to wait until I am dead to see if the corpus really lasted that long.

In these more than 2 years of my retirement, my corpus has always lagged my minimum projections. All thanks to the poor returns of market since 2018. Now, if the market and hence my corpus continues to grow at this slow pace, will I be able to stay retired? Lets find out.

Projections

Let's first start with my projections. I made 3 types of projections for my corpus. They are conservative, aggressive and then something in between. For the conservative projection, I assumed an inflation rate of 8% and investment return of 8%. For the aggressive projection I used 4% inflation and 12% return and for the in-between one I used 6% inflation and 10% return. You know what my real expenses are, but to simplify, lets say my expenses are Rs. 6 lakhs per year. Then using 4% rule, I would need Rs. 1.5 crores by the time I retired in 2018. These are not my real numbers, but lets just go along with the story shall we?

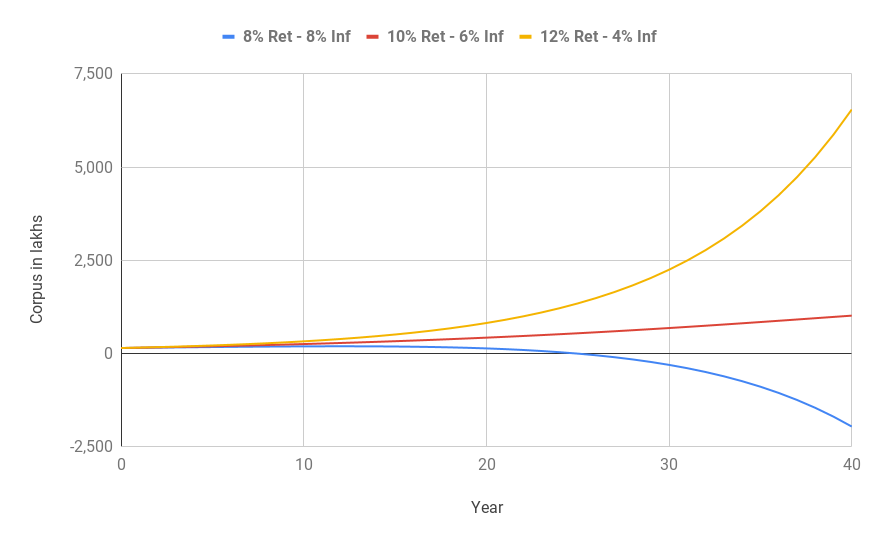

Using the numbers mentioned above, a 40 year projection of my corpus (after compensating for expenses) will look like so.

It is hard to see in the image, but the blue conservative line crosses over the x-axis into negative territory at around 25 years after retirement. Which basically means that I will run out of money in 25 years if my returns are 8% and inflation is 8%. The red line is what I am hoping I can make. Where are the orange line is the aggressive projection. Note that neither the red line or the orange one ever intersect the x-axis in 40 years. It is indicating that my corpus will easily support my expenses with inflation for 40 years.

The reality

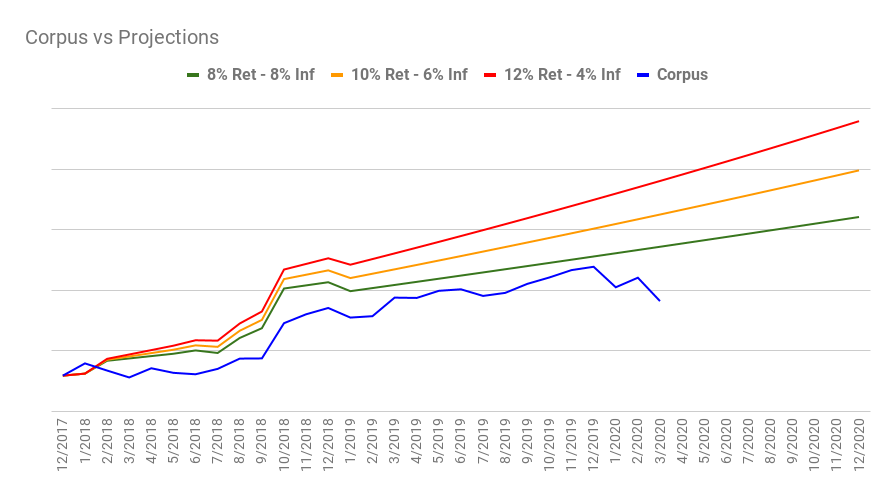

Of course you can project what you like, but things can be different when the rubber meets the road. In my case, the returns of my corpus from Jan 2018 until before the market crash in March 2020 was a lousy 4.78%. If I assume 8% inflation, then I would run out of money in less than 20 years assuming a 4.78% return for all of the future. Thankfully though, my inflation so far has been 0% which can offset the negative effects of poor returns. I am sure my inflation will not stay so low for ever. Anyway, here is the projection + reality until March 2020.

The uneven projections are a result of repayment of home loan, income from PF, final payment from my company when I quit, some money I lent out to parents etc. After Jan 2019, there is no additional income or loan repayment so the projections are much smoother. You will notice that my corpus (after expenses) which is the blue line above, is even below the conservative projection (the green line). Is that cause for worry? Will my corpus last the rest of my life or should I go back to work?

COVID has all the answers

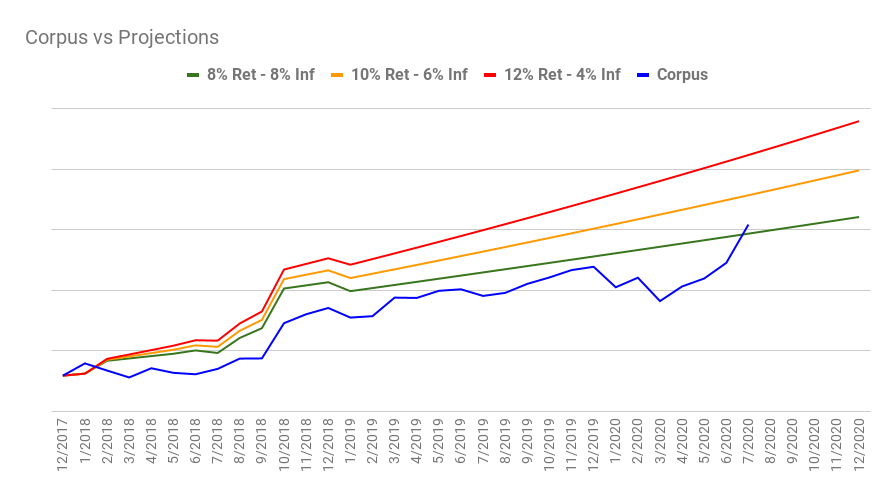

While COVID-19 has beaten down the markets in March, they made a surprise comeback from the lows soon after. So by July 2020, my corpus is up and for the first time since my retirement, broke above the conservative projection. Phew!

I am not sure what the future holds and this may be the last time I will see my corpus above any projection ;). The point I am trying to make is that while my corpus grew well below even my most conservative projection, it did not bother me. The reason is that I did not build a corpus that is exactly 25 times my expenses (the 4% rule). Instead, I have sufficient buffer in the corpus. Which is also the reason I suggest you have 20-50% more corpus than you require. So keep the buffer when making your retirement corpus calculations.