How to Choose a Debt Mutual Fund

Hopefully you have read my post on how to choose a mutual fund. This post is kind of an extension to it. I will specifically explain what things you need to look for when picking a debt mutual fund as opposed to the general advice given in the other post. While I don't consider myself an expert, I will give you some tips based on my experience. But first, the usual disclaimer:

Disclaimer: Information provided in this blog is to help educate you. Any mutual fund, company or stocks mentioned within the post are used only as examples, and should not be considered as recommendations or advice. Use the information to improve your knowledge, and make decisions based purely on your understanding. I may or may not have owned, or still own the names mentioned in this post at the time of writing. I am not your financial adviser, so you are liable for risks arising due to any financial decisions that you make based on methods discussed here.

I assume you have already decided on how you want to split your investment between equity and debt. If you are eligible for Senior Savings Citizen Scheme, go for it first. The next step is to figure out which debt funds to invest in. My first advice in this matter is that you choose only funds between ultra short term and short term debt funds and no other category of debt funds. Don't go for dynamic bond, gilt, credit risk or one of the other 16 bond funds categorized by SEBI. Keep it simple unless you really know what you are doing. Debt funds have a place in your portfolio for a reason, and the reason is to reduce volatility. Funds between ultra short term funds and short term funds have low volatility while giving you better returns than fixed deposits. By investing in these categories of debt funds, you side step interest rate risk to a certain degree. Most other debt funds come with some kind of risk or the other, such as interest rate risk (Gilt), inflationary risk (overnight funds), risk of market cycle (credit risk funds), not sufficiently diversified (PSU and Bank funds) etc.

So what funds fall between ultra short term and short term debt funds? These are the 4 fund categories --

- Ultra short term funds

- Low duration funds

- Money market funds

- Short duration funds

I don't have any more investments in short term or low duration funds today, but I did invest in those funds in the past. I have kept it really simple and have only two ultra short term fund and one money market fund from the above list.

Disclosure: I still do have a few PSU, corporate bond funds and other bad debt fund investments that I have made in the past. I intend to clean up once the new financial year rolls in and I get the tax benefits.

With the categories of fund out the way, the next important thing you want to remember is to keep the expectations low on the returns. The debt funds typically give you 1% more than fixed deposits. Don't expect a huge return, especially given that the inflation is targeted to be around 4%.

The next thing you want to look for is liquidity. While large net assets is a bane for most equity funds, it is a boon in the case of debt funds. You should try and choose funds that have large assets. The advantage is that when lots of people want to redeem from a fund (for example during a crisis), the NAV does not take a big hit since there will be enough liquidity in the market to sell high quality papers. A fund with small net assets will struggle to sell at a good price and consequently the NAV will come down as the fund is forced to sell bonds at a low price since there are very few takers. With this information, you can short list a bunch of funds sorted by net assets, in a particular debt category, for example ultra short term funds.

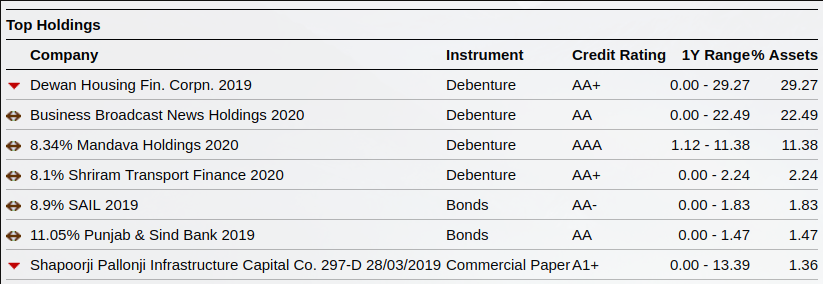

A good starting point is Rs. 5000 Cr for net assets. Okay, you have more or less eliminated most risks, but how about default risk? Well, debt funds are risky for a reason and risk of default is one of them. To reduce the effect of default risk, go through each fund that you have shortlisted above and check to see if they have sufficient diversification. Unlike in equity funds, too much diversification is actually a good thing in the case of debt funds. Concentrated bets are very risky. If you see a fund having more than 10% concentration in one company, it is a huge risk if the company defaults. For example, take a look at a fund with 30% exposure to one company in the figure below. That is a huge risk and you don't want to invest in such a debt fund. If the company defaults the NAV of the fund will drop by 30%!

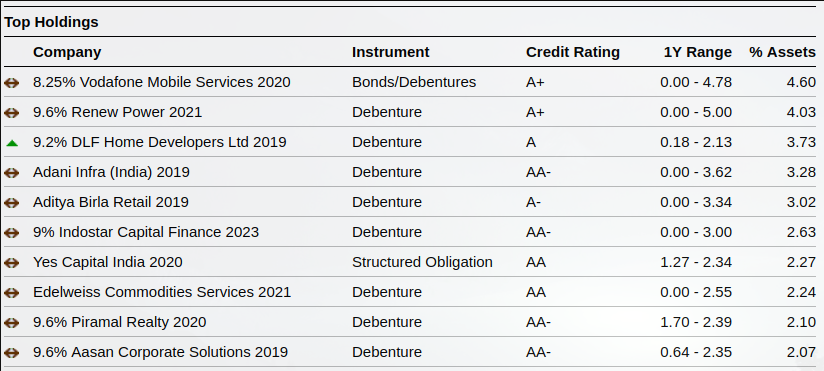

A good fund looks something like the figure below. Don't bother too much about the credit ratings since it is easy to influence the credit rating agencies to give a good ratings. Even a AAA rated IL&FS papers dropped to junk in a quick few months. Always know that some will default and that is the characteristic of a debt fund. Embrace it.

Finally, keep an eye on expense ratio. Short term debt funds don't offer a lot in the way of returns, so you certainly want a fund with low expense ratio. Do the same kind of due diligence for the rest of the debt fund categories you wish to invest in. Select one or 2 funds in each category. You don't necessarily need to invest in all the 4 debt categories. Hope this helps you in picking some good debt funds. Leave a comment below if you have more questions or need clarifications.