How Long Will My Money Last?

How long will your money last? The oft given cliched answer is -- it depends. It is true if you want someone to answer for you. But if you put some effort, you will be able to answer the question yourself. The only problem is that you should be able to make some good estimates of your expenses, inflation and investment return long into the future.

This is a continuation of my earlier post -- How Much Do you Need to Retire. If you haven't read it, I urge you to head over there first. So by now you must have figured out how much you will need for early retirement from my previous post. However, you made your calculations assuming a constant expense (accounted for inflation over your lifetime), a constant inflation rate and a constant investment rate of return. But what if they keep changing depending on what stage in your life you are at? For example, may be at some point in your retirement, your expenses increase because your kid is going to college or you like to travel the world, and the inflation for education or vacation is higher than your initial assumption? The previous calculator could not handle all that.

For folks like you, I prepared a new calculator (at the end of this post) that should help you peek into the future. This calculator has 4 sections called Retirement, X Years After Retirement, Y Years After Retirement and Z Years After Retirement which should help you enter different numbers for different phases of life. The section Retirement needs to be filled according to the instructions from my previous post. The rest of the sections will have to be filled according to the following instructions.

Think of each of the sections as various phases of life. The first section is the first phase when you retire, lets say you retire at 37. Then think of the next phase, may be supporting children's college expenses when you reach 45 years of age. Then the next phase of life, may be you have an empty nest and you only need to support yourself and your spouse, and you both are in good health at around 50 years of age. The next phase is probably your old age from 60 till EOL (end-of-life). These are just examples, you might have phases that are different from this and you can change the numbers as per your requirements.

Corpus

Input your corpus here. This is the amount that you have accumulated or will have accumulated by the time you retire via all your investments.

Expenses per month

Depending on your phase, enter the expense in today's value when you first enter the phase. For example, by default I have used Rs. 70,000 when you enter phase X (perhaps expensive college education increased your expenses in this phase). That number is in present value. The calculator will automatically extrapolate as per inflations used in various sections. In the Y phase I used Rs. 40,000 because now you don't have to support kids so may be it is less expensive to maintain your lifestyle. Finally, in phase Z the expenses increase to Rs. 60,000, perhaps due to higher medical expenses in your old age.

Anticipated age

The age at which you will enter this phase.

Inflation

The expected inflation during this phase. For example in phase X, perhaps the inflation is higher because of college education, and in Y the inflation is lower because it is just food inflation and in Z it is much higher perhaps because of rising cost of medical expenses.

Investment return

You can also play with expected investment returns during each of the phases. Perhaps in the earlier phases you used higher returns because you can take more risks (since you can go back to work if things go south), but as you age you might want to go for a smaller return like in phase Z the return is by default set to only 9%.

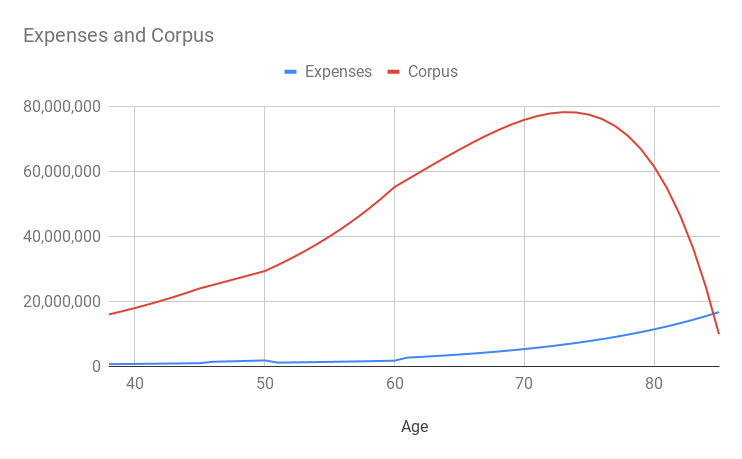

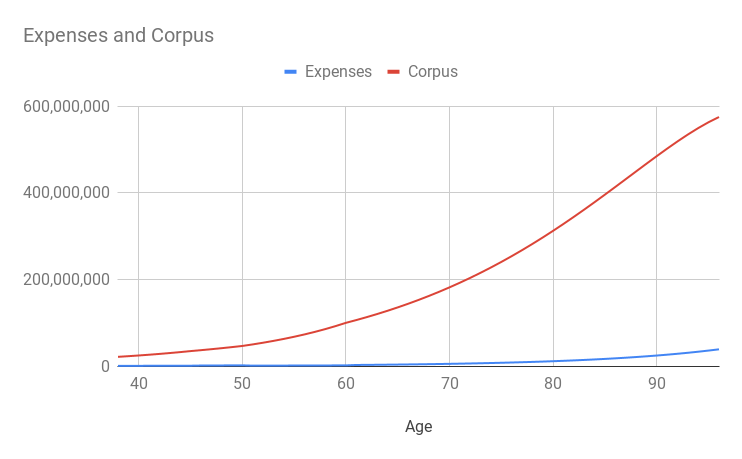

That's it! With those numbers you can see how your expenses and corpus change as you age. If you are worried that you might out live your money, then lower the withdrawal rate a bit in the first section and see how things change. Play with the numbers and have fun!

How Long Will My Money Last Calculator

Retirement |

|

| Corpus | |

| Monthly expenses | |

| Your age | |

| Anticipated retirement age | |

| Inflation | |

| Investment return | |

X Years After Retirement |

|

| Expenses per month (in today's value) | |

| Anticipated age | |

| Inflation | |

| Investment return | |

Y Years After Retirement |

|

| Expenses per month (in today's value) | |

| Anticipated age | |

| Inflation | |

| Investment return | |

Z Years After Retirement |

|

| Expenses per month | |

| Anticipated age | |

| Inflation | |

| Investment return | |

| You will run out of money at this age | |