Am I Financially Ready To Retire?

Here is an alternative take on whether you are financially ready to retire. In this post, I want to help you determine if you are ready to quit with nothing but a simple calculator and just one formula. You don't need to predict expenses, inflation, rate of return etc, and as such, this method is not as comprehensive as the How Soon Can I Retire calculator. So take it with a pinch of salt and use it more as an indicator of whether you are ready to retire or not. Also note that this is only to check if you are financially fit to retire and has nothing to do with your emotional state of mind. Some may have a lot of money and yet cannot retire due to various other reasons (including not knowing what to do post retirement, fear of boredom, peer pressure, family disapproval, social status etc).

The Calculation

Open a calculator and punch in the amount that you have already invested for the purpose of retirement (if you don't have such an investment, then are you sure you are reading the right blog?). As an example, lets say, I have an investment of Rs. 1.5 crore (this includes equity and debt mutual funds, stocks, fixed deposits, PF, PPF etc). The number need not be exact, some rough number will do. Now multiply that number with 10% since I am assuming you can generate a 10% return on your investment, especially if you follow the 70:30 allocation. That is the annual interest on your investment. Now divide the number by 12 to find your monthly return. If this number is more than your monthly salary (assuming you are happy with your salary and able to meet all your expenses easily and have enough left over to sock away for retirement) then you can retire now!

With the previous example that number would be

Rs. 1,50,00,000 * 10 / 100 / 12 = Rs. 1,25,000

So, if I were earning Rs. 1.25 lakhs per month pre tax or about Rs. 1 lakh post tax, and that covers all my expenses and saving requirements then I am all set. As I said earlier, this is a simplified version of the actual calculator and should be used only as an indicator. Go for the full calculator to be sure.

How does that really work? Well think of it this way, if you are able to save enough with your current salary to create a corpus that can generate a second and equal salary, then removing one salary component will leave you with another salary that will meet your current expenses and also save for the future to counter any inflationary effects. But of course this is too simplified and does not account for any big expenses like child's education or huge medical bills. You are supposed to maintain separate corpus for each of those goals and do proper asset allocation based on the duration of the goal.

Example

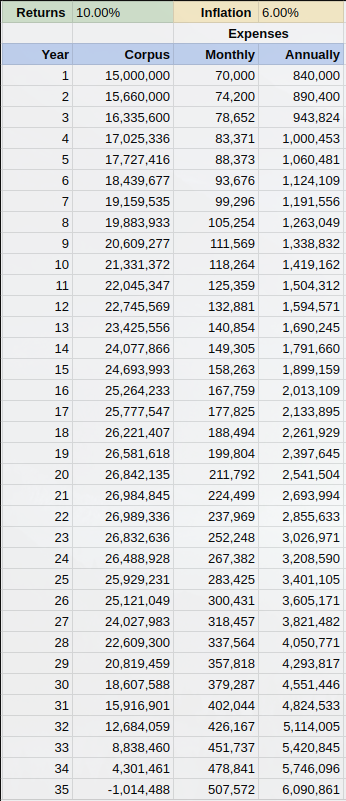

Let me run some numbers for you to help better understand it. Suppose I was earning Rs. 1,25,000 per month and after taxes, I am left with Rs. 1,00,000. I use Rs. 20,000 for EMI, Rs. 50,000 for household expenses and Rs. 30,000 as savings. If I stop earning and decide to live off of my investments of Rs. 1.5 crore, then in the first year I would withdraw Rs. 1 lakh each month and do an SIP of Rs. 30,000 back to the corpus. I use the rest of Rs. 70,000 to cover my expenses. But what about the taxes you ask? Well, after retirement, your taxes will be almost zero, at least for the initial years. I will explain why in a bit, but for now you are effectively withdrawing Rs. 70,000 per month or Rs. 8.4 lakhs per year. By the end of the year, your corpus will have grown by 10% and you would have used up Rs. 8.4 lakhs of it, so you end with up Rs. 156.6 lakhs. Your investment actually grew from Rs. 150 lakhs to Rs. 156.6 lakhs after first year.

For the second year, assume an inflation of Rs. 6%. So you will need Rs. 74,200 per month to meet your expenses as opposed to Rs. 70,000 you needed in your first year. Again we repeat the process. The investment grows by 10% and we take out Rs. 8.9 lakhs to cover the annual expenses and finally left with Rs. 163.35 lakhs by the end of the year. You can probably see how this is progressing. The corpus keeps growing each year by a little bit even as you are withdrawing from the corpus. That works because you are withdrawing less than the interest generated from the corpus, in effect a sort of saving something to cover for the inflation. But this will not go on for ever and the inflation will catch up to the point that the corpus will start dwindling after sometime (see image below). But if you follow this example, your corpus should last 35 years.

This method will only work if you are a good saver and your corpus was a result of your sweat and hard work. It will not work if you inherited a large sum as a retirement corpus. In the example, the saving rate was 30% (savings of Rs. 30,000 from an income of Rs. 1,00,000). Incidentally, your corpus will last longer if your saving rate is higher. Likewise it will not last as long if your saving rate is less. For example, if your saving rate was 20%, then you will run out of money in 28 years instead of 35 as in the example.

Taxes

Coming back to the point I made earlier about taxes, you will barely pay any tax after retirement since you will be withdrawing more of your investment than the interest, at least in the initial years of retirement. It is hard to explain, but let me try anyway with an example. Suppose you started your investment some 20 years ago with Rs. 10,000 per month and increased the SIP every year by 10%. Also assume that the returns of your investment is 10%. That is, if the NAV of the fund you invested in was Rs. 10 in one year, then the NAV will have grown to Rs. 11 the next year and Rs. 12.10 the next year and so on. Then your investment history will look like so

| Year | Investment | NAV | Units | Total Units | Corpus |

| 1 | 120,000 | 10.00 | 12,000 | 12,000 | 120,000 |

| 2 | 132,000 | 11.00 | 12,000 | 24,000 | 264,000 |

| 3 | 145,200 | 12.10 | 12,000 | 36,000 | 435,600 |

| 4 | 159,720 | 13.31 | 12,000 | 48,000 | 638,880 |

| 5 | 175,692 | 14.64 | 12,000 | 60,000 | 878,460 |

| 6 | 193,261 | 16.11 | 12,000 | 72,000 | 1,159,567 |

| 7 | 212,587 | 17.72 | 12,000 | 84,000 | 1,488,111 |

| 8 | 233,846 | 19.49 | 12,000 | 96,000 | 1,870,768 |

| 9 | 257,231 | 21.44 | 12,000 | 108,000 | 2,315,076 |

| 10 | 282,954 | 23.58 | 12,000 | 120,000 | 2,829,537 |

| 11 | 311,249 | 25.94 | 12,000 | 132,000 | 3,423,740 |

| 12 | 342,374 | 28.53 | 12,000 | 144,000 | 4,108,488 |

| 13 | 376,611 | 31.38 | 12,000 | 156,000 | 4,895,948 |

| 14 | 414,273 | 34.52 | 12,000 | 168,000 | 5,799,816 |

| 15 | 455,700 | 37.97 | 12,000 | 180,000 | 6,835,497 |

| 16 | 501,270 | 41.77 | 12,000 | 192,000 | 8,020,316 |

| 17 | 551,397 | 45.95 | 12,000 | 204,000 | 9,373,745 |

| 18 | 606,536 | 50.54 | 12,000 | 216,000 | 10,917,656 |

| 19 | 667,190 | 55.60 | 12,000 | 228,000 | 12,676,611 |

| 20 | 733,909 | 61.16 | 12,000 | 240,000 | 14,678,182 |

Now, after you have retired, lets say you withdraw Rs. 8,40,000 which you can use for your expenses for the first year in retirement. At this time the NAV of the fund is Rs. 67.28 (10% more than the year 20 NAV). So you would need to sell 12485.14 units. That is 12,000 units from year 1 at NAV of Rs. 10 and 485.14 units from year 2 with NAV of Rs. 11. Next we take indexation benefit. Lets assume 6% indexation per year. From year 1 to year 21, it is 20 years of indexation at 6% which is 3.2 (1.06 20) times the year 1 value. And for year 2 it is 3.03 times. Your total cost of investment then becomes

Rs. 10 x 3.2 x 12000 + Rs. 11 x 3.03 x 485.14 = Rs. 4,00,169

Of the Rs. 8,40,000 that you sold, only Rs. 4,39,831 is your capital gain. After taking the basic exemption limit of Rs. 2,50,000 as per current tax slabs, you are left with paying 20% capital gain tax on Rs. 1,89,831 = Rs. 22,779, which is less than Rs. 2000 per month lost in taxes. If you had split your investments into multiple folios, and sell some short term investments and invest in ELSS you could save even more taxes. But that is a lot more complex, but doable and an exercise for you, or may be I will write another post some other day.

Anyway, this was a layman's way of figuring out if you are ready to retire. Agree or disagree? Let me know in the comments below.