Should You Sell Debt Or Equity For Retirement Expenses

After reading my post on “withdrawal plan in retirement”, one reader asked why I suggested that one should sell debt mutual funds to handle the retirement expenses. In that post I gave an example where an investor has only debt and equity mutual funds and in that scenario, it is preferable to sell debt mutual funds to handle everyday expenses and then do a rebalance once in a while to get the asset allocation to the ratio that you prefer. The reason for this recommendation is quite simple. It is to avoid selling mutual fund units of an asset class at their low point. Since equity mutual funds go up and down quite a bit in value, it is possible that in some years you might sell at a low point and dent your compounding effect. I will explain how with an example.

Suppose your monthly expenses are Rs. 1 lakhs, which is Rs. 12 lakhs in a year. You take out full annual expenses money from your investment at the start of each year. Lets say your fixed income part of the portfolio which is debt mutual funds gives a return of 6% per annum. Now, imagine this situation where there are 3 consecutive years of negative returns from equity. Say -10% each year. After that, equity returns are a solid 10% each year for the next 7 years. I know this is a hypothetical situation, but lets just go with it anyway. Finally, to keep things simple, lets say inflation is 6% every year. Assume 60%:40% asset allocation to equity and debt.

Before making the calculations, I’d like to explain mutual fund units, because it is an important concept to know before understanding the calculations below. Whenever you purchase mutual funds, whether it be equity or debt mutual funds, what goes out (debited) from your account is money and what comes in (credited) is a bunch of units of the mutual fund you purchased. Suppose you spend Rs. 1 lakh to buy units of a mutual fund whose NAV (net asset value) is Rs. 1,000. Then what you get is 100 units of the mutual fund.

Money spent = Rs. 1,00,000

NAV of MF = Rs. 1,000

Units bought = Rs. 1,00,000 / Rs. 1,000 = 100

Now, lets say after 1 year, due to various market conditions, the mutual fund value went up by 10%. What do you think will change to reflect that increase in value? It is the NAV. The NAV will go from Rs. 1,000 to Rs. 1,100 (10% gain). The number of units you hold is still 100, assuming you did not sell anything in that year. So your investment has become Rs. 1,10,000 in imaginary form. It is only real when you actually sell the units. So your imaginary gains are Rs. 10,000.

Money spent = Rs. 1,00,000

NAV of MF = Rs. 1,100

Units you own = 100

Current value = Rs. 1,100 x 100 = Rs. 1,10,000

Profit = Rs. 1,10,000 - Rs. 1,00,000 = Rs. 10,000

Likewise, if the market went down by 10%, then the NAV would have gone down to Rs. 900 and you would have a notional loss of Rs. 10,000. Basically your gains or losses are based on the NAV and the units you own. Now on to the example.

Using debt funds for expenses

Suppose you invested only in one debt and equity mutual fund and the NAV of both the mutual funds is Rs. 1,000. Assuming you have Rs. 600 lakhs, you would have invested Rs. 240 lakhs in debt mutual fund and Rs. 360 lakhs in equity mutual funds. Then your portfolio will look like this

Debt MF NAV = Rs. 1,000

Debt MF units = Rs. 240 lakhs / Rs. 1,000 = 24,000

Equity MF NAV = Rs. 1,000

Equity MF units = Rs. 360 lakhs / Rs. 1,000 = 36,000

If you sold debt mutual funds to fund your retirement expenses, then you need to sell enough units at MAV of Rs. 1,000 to get Rs. 12 lakhs. So you will be selling 1,200 units.

Expenses = Rs. 12,00,000

Debt MF NAV = Rs. 1,000

Debt MF units sold = Rs. 12,00,000 / Rs. 1,000 = 1,200

Debt MF units left = 24,000 - 1,200 = 22,800

Debt MF value = Rs. 1,000 x 22,800 = Rs. 228 lakhs

Equity MF NAV = Rs. 1,000

Equity MF units left = 36,000

Equity MF value = Rs. 1,000 x 36,000 = Rs. 360 lakhs

Say one year has passed and your debt MF grew by 6% and equity MF grew by -10%. Then your portfolio becomes

Debt MF NAV = Rs. 1,060

Debt MF units left = 22,800

Debt MF value = Rs. 1,060 x 22,800 = Rs. 241 lakhs

Equity MF NAV = Rs. 900

Equity MF units left = 36,000

Equity MF value = Rs. 900 x 36,000 = Rs. 324 lakhs

Corpus = Rs. 241 lakhs + Rs. 324 lakhs = 565 lakhs

Suppose you rebalanced your portfolio to 60:40 ratio, then your portfolio will look something like this.

Debt MF value = Rs. 565 lakhs x 40% = Rs. 226 lakhs

Debt MF NAV = Rs. 1,060

Debt MF units = 21,320

Debt MF value = Rs. 565 lakhs x 60% = Rs. 339 lakhs

Equity MF NAV = Rs. 900

Equity MF units = 37,667

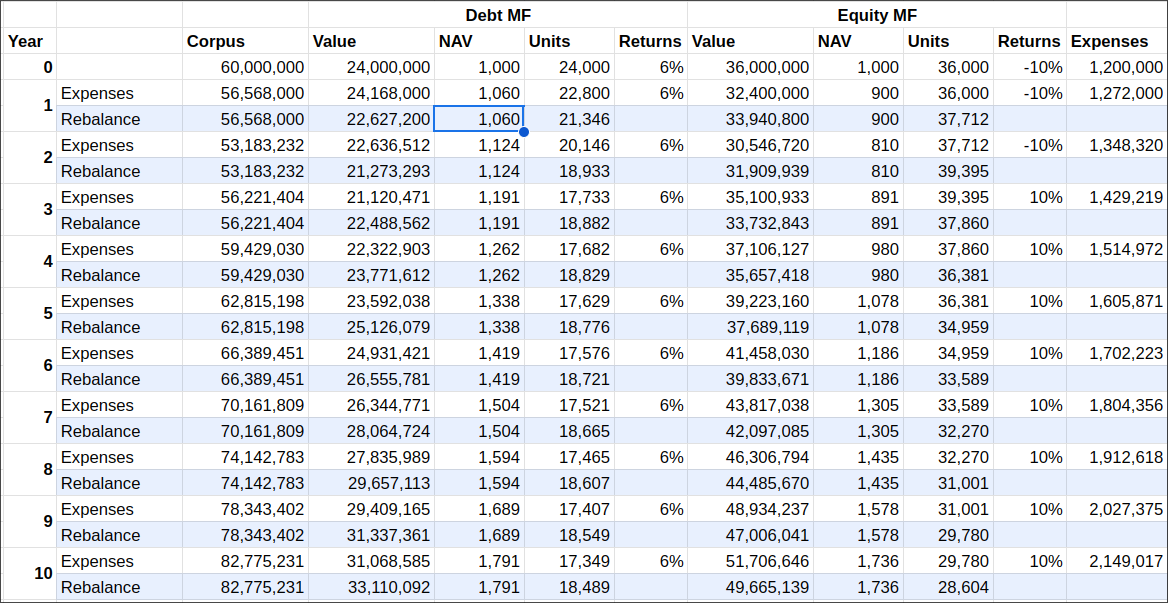

If we keep doing the same thing for the next 10 years, your corpus would look something like this

Notice that you end 10th year with a corpus of Rs. 827 lakhs.

Using equity funds for expenses

Now if we perform the same routine but selling equity MFs, how would it look like?

Seems like we end the 10th year with pretty much the same corpus. Which tells us that it does not matter which asset class you want to sell to fund your expenses, the rebalancing will take care of keeping the portfolio in balance. So in conclusion, I stand corrected that you need to sell only debt mutual funds. It seems more of a psychological aspect than anything else. Feel free to sell which ever asset class you prefer and as long as you are rebalancing, things will work out fine. I learned something new in the process, so thanks for asking the question :).