The Gilt Experiment

You've probably heard about the inverse relationship between bond prices and interest rates. When interest rates rise, bond prices fall and vice-versa. How can we use this information to make some money without a lot of volatility? Read along about my experiment with interest rate cycles.

Disclaimer: I would not advice anyone to take risks like I am about to explain in this post. It is supposed to be more of a study rather than any recommendation or advice. Any mutual fund names discussed here are purely for the study of the experiment and not a recommendation.

The Entrance

It was the June of 2014 when I decided to run an experiment to figure out if the bond price to interest rate relationship is useful at all. To be able to run the experiment, one has to understand interest rate cycles and know where in the cycle the current interest rate stands.

Something interesting happened in January of 2014 when the then deputy governor of RBI, Urjit Patel suggested that inflation should be the nominal anchor for the monetary policy framework. And the target for inflation is set as 4 per cent with a +/- 2 percent tolerance around it. RBI wanted to curb the inflation to 8% in the next 12 months, to 6% in the following year, and then have it be stable around 4% from then on. The 8% interest rate at the time was at almost the highest in more than 10 years. Oil prices were at highs and starting to come down. I felt that the inflation will go down, and hence the interest rates will go down along for the ride, which means bond prices will go up. A good time to invest in bonds.

If the economy stays on this course, further policy tightening will not be warranted. On the other hand, if disinflation, adjusting for base effects, is faster than currently anticipated, it will provide headroom for an easing of the policy stance.

Second Bi-Monthly Monetary Policy Statement, 2014-15

Retail inflation measured by the consumer price index (CPI) has eased for the second consecutive month in June, with a broad-based moderation accompanied by deceleration in momentum. Higher prices of vegetables, fruits and protein-based food items were offset by the muted increase in the prices of non-food items, particularly those of household requisites and transport and communication. CPI inflation excluding food and fuel decelerated further, extending the decline that began in September 2013.

The recent fall in international crude prices, the benign outlook on global non-oil commodity prices and still-subdued corporate pricing power should all support continued disinflation

Third Bi-Monthly Monetary Policy Statement, 2014-15

Since retail investors cannot invest directly in bonds, I went the mutual fund route via Gilt funds. Gilt funds invest in low-risk debt such as government securities, central government loans and state development loans of medium to long-term horizon, which ensures the preservation of capital. The important thing to note is the duration of these loans, which is medium to long term. The longer the duration, the higher the interest rate sensitivity. Hence I started investing in a couple of Gilt Mutual Funds from June 2014.

The Exit

Although RBI did not immediately start reducing interest rates, I started my SIPs and continued on. Eventually the cuts started happening and NAV of Gilt funds kept going up. I was a happy camper.

Then in June 2017 I stopped my investment (and the experiment) when I felt that the interest rate has hit the bottom of the cycle and I should get out as RBI has kept the rates unchanged for 3 bi-monthly meetings and had a neutral or positive economic outlook. However, RBI went on to do one more cut after I decided to get out.

The decision of the MPC is consistent with a neutral stance of monetary policy in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Minutes of the Monetary Policy Committee Meeting June 6-7, 2017

The Results

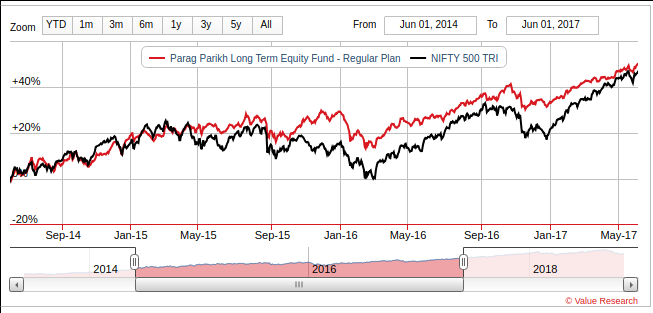

So how did the experiment go? Well, it was good but not great. It was not a failure because it served the intended purpose, but I could have done better following the beaten path. Let me explain. At the end of the experiment, I made an annualized return of 11.87% over those 3 years (after the 20% tax on capital gains after indexation, it will be a bit lower than that). Instead, if I had invested the same amount in a good multi-cap fund I would have made 13.79% during that time.

Source: Value Research

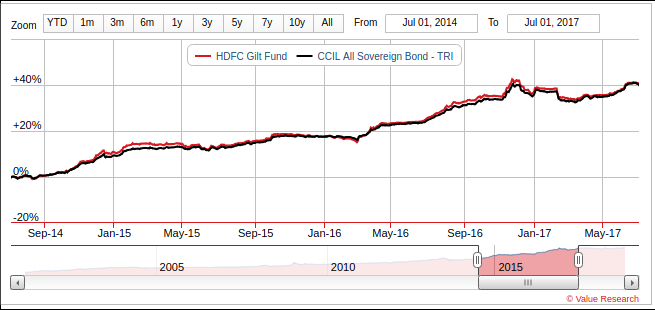

In fact, if I had just followed my 70:30 rule blindly, I would have made a 12.25% return. So why is this not a failed experiment? Because the experiment did prove that you could get double digit returns even from debt funds and not just equity, which is what I set out to prove. Moreover the returns were not too far from my 70:30 rule, but the most important thing was that the volatility is much lower compared to equity as you can observe from comparing the following graph with the previous one.

Source: Value Research

To get the most out of the interest rate cycle, one should know when the cycle starts and ends. The interest rate cycle is a bit more predictable than market cycles, but predicting the top and bottom of any cycle is hard. More importantly, you need to keep up with the news, RBI stance and macro economics. If you don't know how to time the interest rate cycle, but want to participate in it then you could try the dynamic bond funds (yes, there is a mutual fund for that) and leave the timing part to a fund manager. But what is the fun in it :)?

Moral of the story? Stick with 70:30 rule irrespective of market conditions and don't follow any fancy ideas. I probably would not do the interest rate cycle timing again in the future.