Should You Prepay Loan Or Invest?

When you have some savings you might wonder whether to invest the savings or prepay your loan. I have always suggested a simple thumb rule, which is that if you anticipate your investments to give you better returns than the loan interest rate then invest, otherwise prepay your loan instead. Generally, for almost all kinds of loans the return on investment is usually lower than the loan interest. One exception is home loan which has a much lower effective interest rate because you get tax benefits. For most other loans it is better to prepay. That is a very simplistic rule, but does it really work? Let’s find out.

A usual question that comes up when someone asks me for financial advice, is whether they should prepay a loan or invest any excess money that they have saved up. I generally give them the simple advice that they should look at the interest rates of investments and loan and see which one is higher. If return on investment is better then they should invest. Otherwise they should repay the loan. Then I thought why not make a spreadsheet to clarify this simple rule so they can check for themselves? Which is exactly what I did.

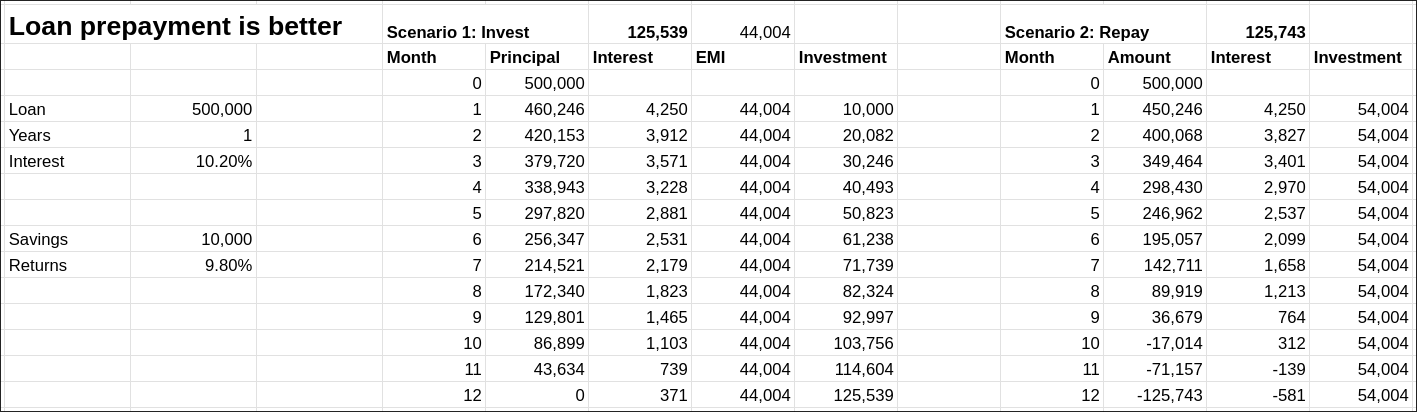

You can try it out yourself by making a copy of my spreadsheet and changing the numbers to fit your needs. When you enter your numbers, the B2 cell will tell you what you should be doing. For example let’s say I have a loan of Rs. 5L for 1 year at the interest rate of 10.2%. Also assume that I can save Rs. 10,000 every month after taking care of all expenses including all my EMIs. Further, assume that I anticipate a return on investment of 9.8%. Should I invest the Rs. 10,000 every month, or should I prepay my loan? According to the spreadsheet, given the numbers above, it tells you that it is better to prepay loan instead of investing.

In the spreadsheet you can change the following

- loan value

- number of years

- loan interest rate

- savings

- investment returns

The calculations will be based on that information. Of course, this may not be how it is in the real life because there will be some expenses related to prepaying the loan. For example, some loans require you to wait a few years before you can even prepay. Most loans will charge you a fees for prepayment. So if you add up all those costs, the prediction may be different from the reality. Still it is a good guideline.

What the spreadsheet suggests is that my simple thumb rule makes sense. For example if you set the investment returns to be the same as the loan interest rate then the spreadsheet will tell you that either way is fine because at the end of the loan period you will end up with the same amount of investment whether you prepay or invest. In the case of prepayment, it is assumed that once your loan becomes zero, any additional savings including the amount you might be paying for EMI will be invested.

The biggest problem in this whole exercise is not what you should be doing with your savings, by predicting the future returns. How can you be sure whether you future investment returns will be better than your loan interest? There is no easy way to do that analysis. My very rough guideline for expected returns is what and FD would give you (about 7% at the time of writing this post) if the investment period is 3 years or less. For investment that is more than 7 years, you can go with average long term equity returns which I say is about 12%. For the in between years, you can expect something that is in the middle of those two returns. So about 9-10% today.

As you can see, it is not a very cut and dry kind of situation, especially in the grey area of 3-7 years. Even after 7 years, the possibility of earning 12% is not always guaranteed. Finally, even below 3 years there is possibility of RBI tweaking the rates which will affect the FD rates. So realistically, you cannot put an accurate number for the return on investment. It will always be a guessing game. Hence I suggest that you go with a lower expectation.

In most cases you cannot really beat the loan interest rates, so I almost always suggest everyone to clear their loans first and then think about investing. The only exception, as I mentioned before is if you have a home loan. Home loans tend to have lower interest rates because the bank has a collateral and on top of that, you get two kinds of deductions in the old tax regime. You get deductions for the principal payments up to Rs. 1.5L per year in addition to the Rs. 2L deductions for the interest payments. Those deductions alone reduce the effective interest rate of the home loan further. Hence you can continue paying EMIs for home loan and invest the savings in long term investments.