How Much Did Franklin Ultra Short Term Fund Return

It has been more than a year and a half since Franklin Templeton India sent out that email letting investors know that it is winding up six debt mutual funds. There was a lot of uncertainty at the time and many people were worried that they might lose their investments. Nothing of that sort has happened and we got back most of it. There is still some more to come, but at least people are confident that they will get back their full investment. That is also the reason that we don’t hear much in the news about Franklin anymore. Back in the day you would hear about it pretty much every other week.

I don’t know about others, but I had a huge investment in Franklin Ultra Short Term fund. Almost 40% of my investments were in that fund at the time of winding up. Not just my money but my parent’s money and my wife’s money too was in it. So as a family we had a huge stake :). Thankfully nobody was worried about the investments because I explained them about what happened and when we will get back the money.

To tell you the truth at the time I was expecting that it will be 2027 before we can get back all our investments. The reason was because Franklin India Ultra Short Bond Fund (FIUBF) was holding some papers with a maturity date of 2027. Hence my conclusion that it will take that long. However, in reality it is going to be much sooner than I anticipated.

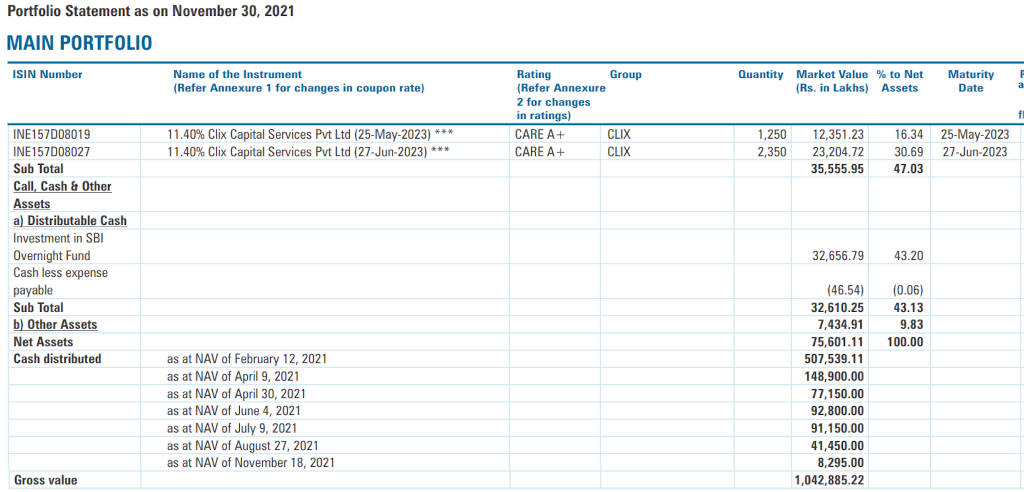

I don’t know about the rest of the 5 funds that are under winding up but with respect to FIUBF, I have already received 99% of my total investment at the value of June 2020. But of course that was just my total investment as on date based on the NAV of June 2020. If I had all that money and invested in another ultra short term fund I would have received some interest on top of it. So if I add a 6% interest to the principal since that time, I have so far received 93%. Not bad at all.

In addition, FIUBF has about 50% of its AUM in cash equivalents which will most likely will be released soon. So only a small portion of our investment is left in some bonds that will mature in 2023. I think that even those bonds will be sold and the money will be returned before 2023. Hopefully this brings some closure to all the investors.

While I am happy that most of my investment is back, I never actually suspected that it will not come back. My main problem is that the funds were sold without my intention to sell them. So I have to figure out all the tax implications and pay tax. This is an unexpected outflow for me and did not go according to the plan. As a result my actual corpus growth was lower than what it would really have been. It is drifting away from my projections. But that is life now isn’t it? Unexpected things always happen and we just have to navigate life as best as we can given what is being thrown at us.

Anyway, I am glad that this whole winding up situation is coming to an end. Soon I will be able to chalk out a new plan for my investments and budget. I was unable to consolidate any of my investments for the past 2 years because of the uneven income from FIUBF. I will probably have one more post after my whole investment is back and then we will call it a wrap :).

Moral of the story is never plan to maximize returns. When it fails, you will not be prepared to handle the situation. You may expect the best outcome, but always be prepared for failures and some loss. Be realistic and remember, what can go wrong will go wrong and you have absolutely no control of the outcome. If the Franklin situation caused even a slight bit of heartburn to you, you should know that you are not adequately prepared. We give to much attention to the work and negligible attention on our expectations. Our expectations are also in our control and we should manage them well.